The Data Shutdown: Learning to Fly, Blind

October 3, 2025

It’s pretty tough to know today where the economy will be tomorrow when we won’t know where it was yesterday until the day after tomorrow. Or the month after tomorrow.

The U.S. federal government shutdown, which began Wednesday, will likely be a small irritant for the economy. It could result in some job losses and be largely ignored by the markets, but will cause some real issues for the Fed. While it’s early days yet, this shutdown has the feel that it could challenge the record five-week episode in 2018. And going a month without official data will force monetary policymakers to make a crucial decision on rates at the October 29 FOMC meeting on the thin gruel of private-sector data. All at a time when there are still many questions over how the economy is dealing with the multitude of policy changes seen in 2025.

After all, it was precisely six months ago that stocks were in full retreat in the moments after “Liberation Day” and all its reciprocal tariff rates. There has been a nonstop series of back and forth announcements on the issue since then—mostly forth—which has left the average U.S. tariff rate around 18%, up from about 2% at the start of the year. And the full impact of that massive shift has yet to land, with only a small share of the increase so far passed on to consumers. That helps to explain why the economy has proven to be resilient in the face of intense uncertainty, as it now looks like GDP growth will be above 2.5% in Q3 following the 3.8% snapback in Q2.

The other reason why growth has held up is a good old-fashioned tech spending boom on all things remotely related to AI. However, even while business investment in equipment has been solid, firms remain highly reluctant to add to payrolls; the no-hire, no-fire economy, as it were. While we did not get the September employment report as planned this week, the ADP release found a 32,000 job loss last month after a 3,000 setback the prior month (revised down from an initial +54,000). This emerging divergence between headline GDP growth and jobs may be a tantalizing hint that productivity is sparking higher, thanks to AI. However, before getting too carried away, note that U.S. productivity growth has averaged just a bit above 2% in the past three years (roughly since ChatGPT burst onto the scene), almost exactly in line with its 30-year average growth rate.

Investors are shrugging off such details, and were quick to look past the shutdown, driving equities to yet new highs this week. The S&P 500 is now up a scorching 35% since the lows hit less than six months ago in early April. And lest you think it’s just the mega tech companies driving the bus, the Russell 2000 small cap index is up by nearly 40% over the same period. True, that’s a very specific starting point, and the year-to-date gains of 14% and 10%, respectively, are much less eye-popping. Even so, a double-digit advance at a time of deep policy uncertainty, rapidly cooling job growth, and somewhat sticky core inflation is quite impressive.

The glue that is holding the market together is the prospect of further rate cuts. Even with the official data void, market pricing is assigning a 97% chance of a 25 bp trim at the upcoming Fed meeting, with heavy odds of a follow-up in December. We largely concur. If anything, the shutdown may have slightly bumped up the odds of a cut, since it will likely clip growth and further dent household sentiment. One of the few major reports that was produced this week saw the Conference Board’s consumer confidence index retreat for a second consecutive month and is well down from a year ago.

As well, the combination of the two ISM reports (arguably the most important and well-respected private economic releases going) pointed to soft activity, with the factory survey nudging up to 49.1, while the services version dipped two points to 50.0 on the button. The latter saw the business activity measure drop below the 50 waterline for the first time since the pandemic shutdowns in 2020, but also saw prices rise further to an uncomfortably hot 69.4. Neither measure is at an extreme, but both are cruising in the general direction of stagflation land, or at least to firm underlying inflation and soft growth. With the shutdown underway, it will be a long time before we know for sure, given the data void. Ending on a positive note, the good news is we won’t hear many more complaints about poor data quality for quite some time!

If anything, the TSX is on an even bigger roll than its major U.S. counterparts, with the index now up 23% since the start of the year and a blistering 60% over the past 24 months. That ranks the current run in the top 7 performances over a two-year period since 1960. True, the stunning run in gold prices and related equities are juicing those returns, but we calculate that even ex-materials, the index is up a solid 15% so far this year (actually nudging out the S&P 500, even without the gold rush).

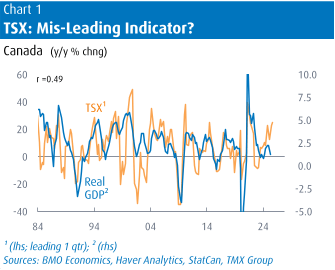

This again raises the question of “how can the TSX be so strong when the underlying Canadian economy is struggling?” The knee-jerk response, including oftentimes from us, is that the index is a pale reflection of the economy. But as Chart 1 suggests, the TSX has actually been a decent early indicator in the past for growth, leading GDP by about a quarter. The relationship is far from airtight: note the wide divergences around the tech boom/bust in the late 1990s/early 2000s, which has some echoes today. But, at the very least, the rollicking ride in stocks suggests that some of the gloom around the economic outlook may be overdone.

Of course, a critical piece in that outlook is where Canada/U.S. trade relations are headed, and we will have much more to say on that topic in next week’s Focus. As well, Prime Minister Carney will be making a second visit to the White House on Tuesday, no doubt with the upcoming USMCA review in sight. Meantime, unlike the U.S., the Canadian economic data machine will still be motoring, with August international trade also out on Tuesday and September jobs on Friday. (The trade data, and thus ultimately GDP, could eventually be affected by the U.S. shutdown, but apparently the August report is ready to roll.) These reports will play a very big role in helping guide the Bank of Canada’s rate decision on October 29, which is much less clear-cut than the Fed. For now, we lean to a short pause, while market pricing is leaning to another 25 bp trim.

Policy Contributing Writer Douglas Porter is Chief Economist for BMO.