Budget 2025: Financing Canada’s Hinge Moment

Shutterstock

Shutterstock

By Kevin Page with Adam Parwana and Hao Tian Shen

October 14, 2025

Budget 2025 will be tabled in Parliament by Finance Minister François-Philippe Champagne on November 4th. It is an opportunity for Prime Minister Mark Carney’s government to set a new policy direction for Canada. Uncertainty is high. Stakes are high. Will the government meet the moment – the hinge moment, as Carney would say? Will Budget 2025 be fiscally responsible?

James Baldwin, the late American writer and activist, said, “Not everything that is faced can be changed. But nothing can be changed until it is faced.” Canada is a great country by many metrics (see Browne and Page, Policy Magazine, 2025). But we are slipping in some fundamental ways.

Work by Nobel economics laureates Daron Acemoglu and James Robinson (Why Nations Fail, 2014) illustrates that successful countries are founded on inclusive institutions that promote opportunities for people, especially the young, to participate in the economy and drive the innovation essential for prosperity.

After 25 years of largely avoidable crises, globalization and technological change, people are losing faith in our institutions and this has been highlighted in research by Statistics Canada. These forces are made even more dangerous by geopolitics in a divided world amid the apparent unravelling of the rules-based international order.

Author Salmon Rushdie describes hinge moments (Languages of Truth, 2021) in history as, “when everything is in flux and the future is up for grabs”. Dan Gardner highlights the implications for sovereignty (“Liberal Democracy is in Danger”, Substack, 2025) “…as uncertainty rises and society frays, freedom feels like a burden”.

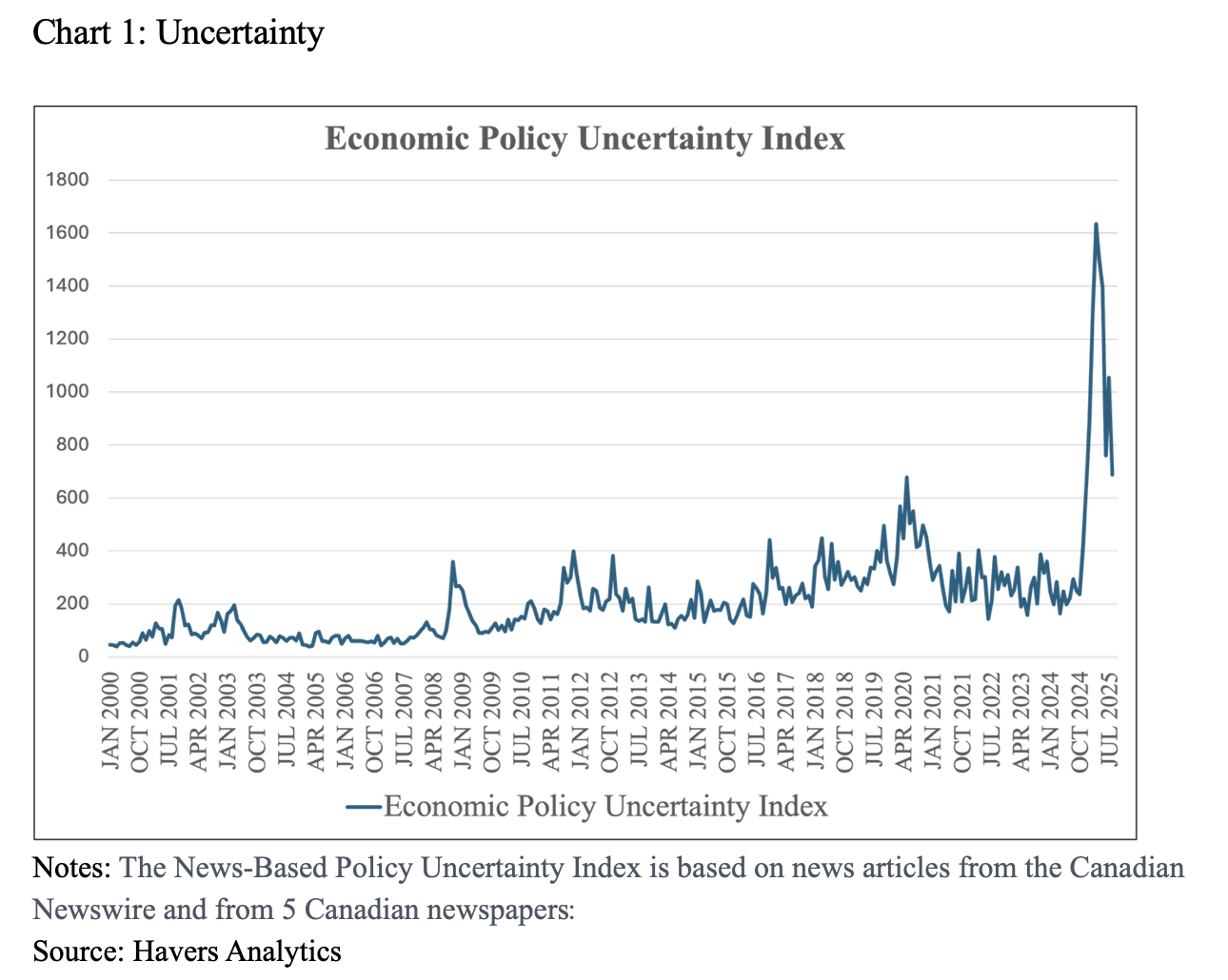

Economic uncertainty is hitting record levels in 2025, higher than the 2008 financial crisis and the 2020 global pandemic. Chart 1 highlights uncertainty reported in Canadian newspapers. On a more global scale, the price of gold, a harbinger for holding value in periods of uncertainty, has doubled to $4000 US per ounce over the past two years.

Budget 2025 must be honest with Canadians about the challenges that have brought us the hinge moment. Per James Baldwin, Canada must face the change. It must provide a new policy vision. It must provide an economic strategy and plan for which Parliament and Canadians can hold the government to account. The fiscal plan must be responsible to current and future generations and reflect the moment of our times.

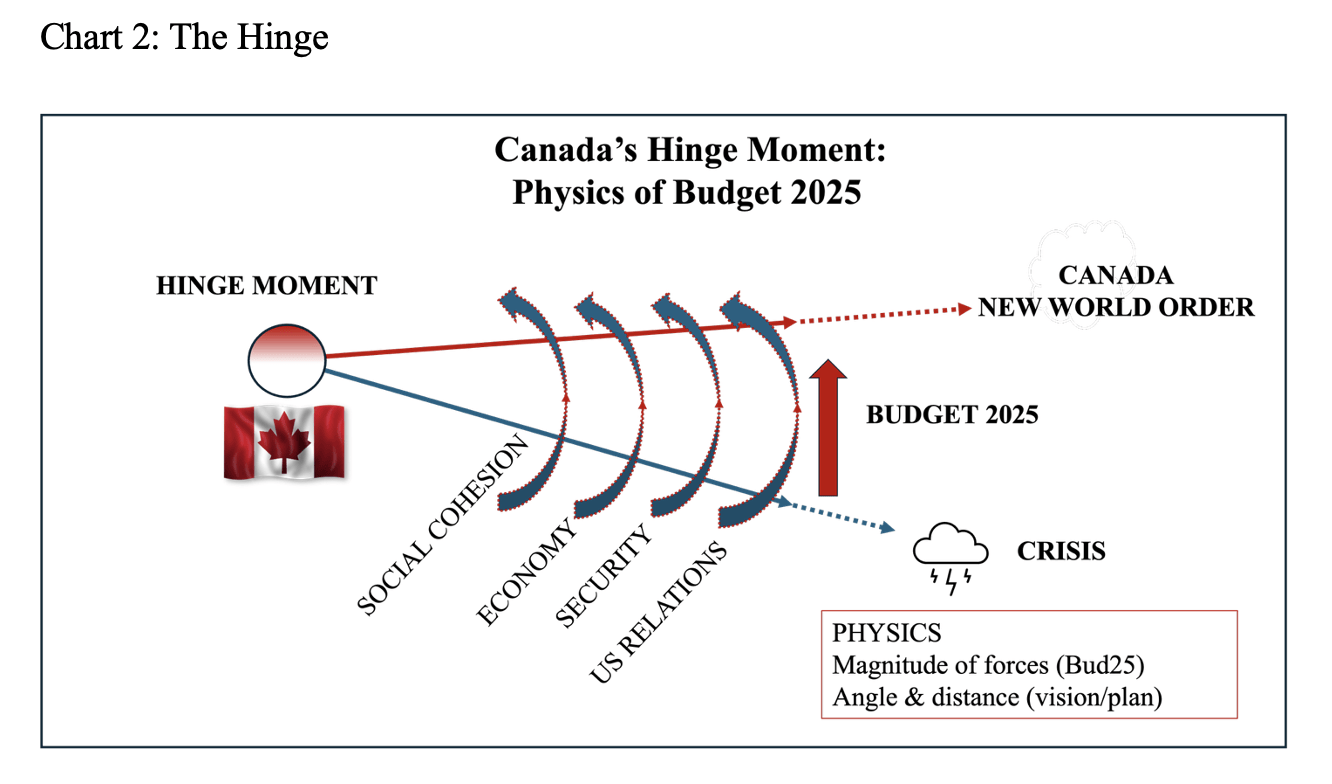

Hinge moments in history, like in engineering, involve forces of change.

Over the past 25 years, we have seen negative forces impacting our collective quality of lives:

- on social cohesion: income and wealth inequality exacerbated by COVID and inflation; large disparities between Indigenous and non-Indigenous well-being; poor performance on reducing carbon emissions; dissatisfaction with health care (wait times); large shortages of affordable housing; more recent affordability pressures with prices for food and energy rising faster than wages;

- on economic growth: weak productivity growth underpinned by weak business investment, innovation, and regulatory barriers; more recent increases in unemployment;

- on national security: underinvestment in national defence relative to NATO commitments and Arctic sovereignty and growing risk from cyberattacks and foreign interference; and

- on US relations: an abrupt fracture in relationship driven by President Trump’s trade policy and threats to Canadian sovereignty; risks made severe by Canada’s overreliance on the US economic market and defence policy.

The 2025 Liberal platform, Canada Strong, laid out a policy agenda for this moment focusing largely on the rupture in relations with the U.S. and ongoing affordability challenges. After a decade of policy enhancements that focused more on issues related to social cohesion (wealth redistribution), the platform and subsequent announcements shifted the policy focus to economic growth (wealth creation) through business investment and trade diversification and addressing NATO targets on national defence.

The challenge for Budget 2025, in this hinge moment, is to articulate that economic vision and plan in a way that builds confidence and trust. If the economic vision and objective is to see Canada as the fastest-growing economy in the G7 over the next five years, what are the strategies and plans on innovation and technology, on industries (resource, manufacturing, etc.), on regulation, on trade diversification, on adjustment (training), on national defence, on public service renewal? How will ‘big’ projects be financed, implemented and monitored?

In engineering, the physics of hinge moments involve the magnitudes of forces. Without forces, there is no torque to generate rotation (a hinge moment). In budget-speak, Budget 2025 must lay out the priorities and policies (forces of change) and the associated resources (weights that generate the force). A hinge moment in history must be resourced (in blood, toil and taxpayer resources). There are no free rides (or rotations) that lead to a better trajectory for the wellbeing of Canadians in a new world order.

While Canada grapples with this hinge moment inside its borders, it must work with other democratic-led countries to reform (and protect) a rules-based international order against the rise of autocratic powers. In response to President Trump’s policies on trade and defence, Canada and other democracies are responding with trade diversification and increased defence spending. As Prime Minister Carney has said, in this hinge environment, when one door closes, another door opens. Will shifts in trade and defence policy be sufficient to counter power plays from autocratic countries? No. They are, however, a necessary first step.

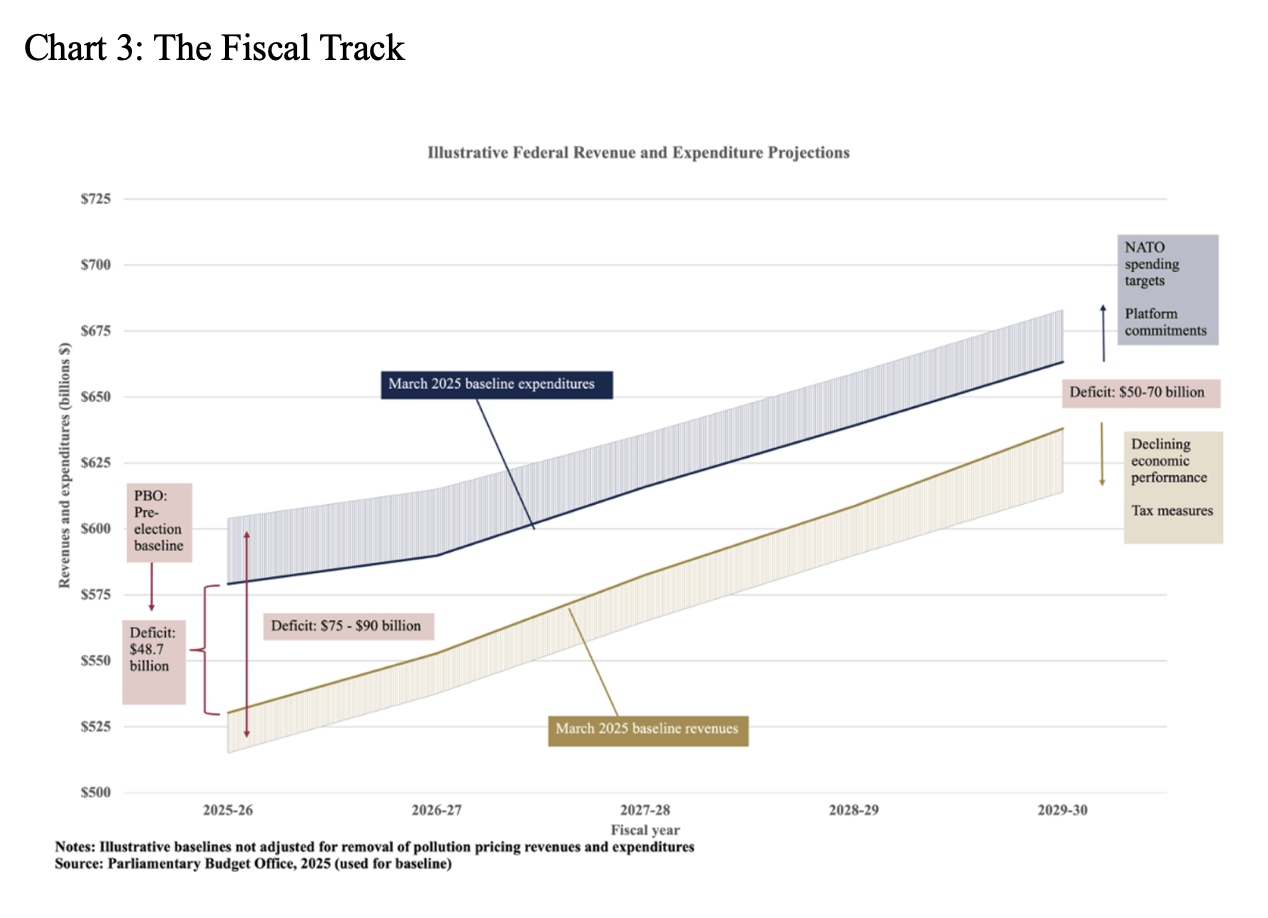

There has been recent, heated debate on Canada’s fiscal situation stirred in part by the PBO release of a pre-budget baseline that shows a federal budgetary deficit increasing to $69 billion in 2025-26 (2.2 percent of GDP) from about $52 billion (1.7 percent of GDP). Thereafter, the deficit track trends down modestly. The debt-to-GDP ratio rises modestly from 41.7 percent of GDP in 2024-27 to 43.7 percent of GDP in 2028-29 and stabilizes. The increase reflects a weaker economic outlook and the implementation of some of Prime Minister Carney’s agenda (but more to come).

Should Parliamentarians and Canadians be concerned about the higher anticipated deficit track? How will the markets and credit ratings react to higher deficits?

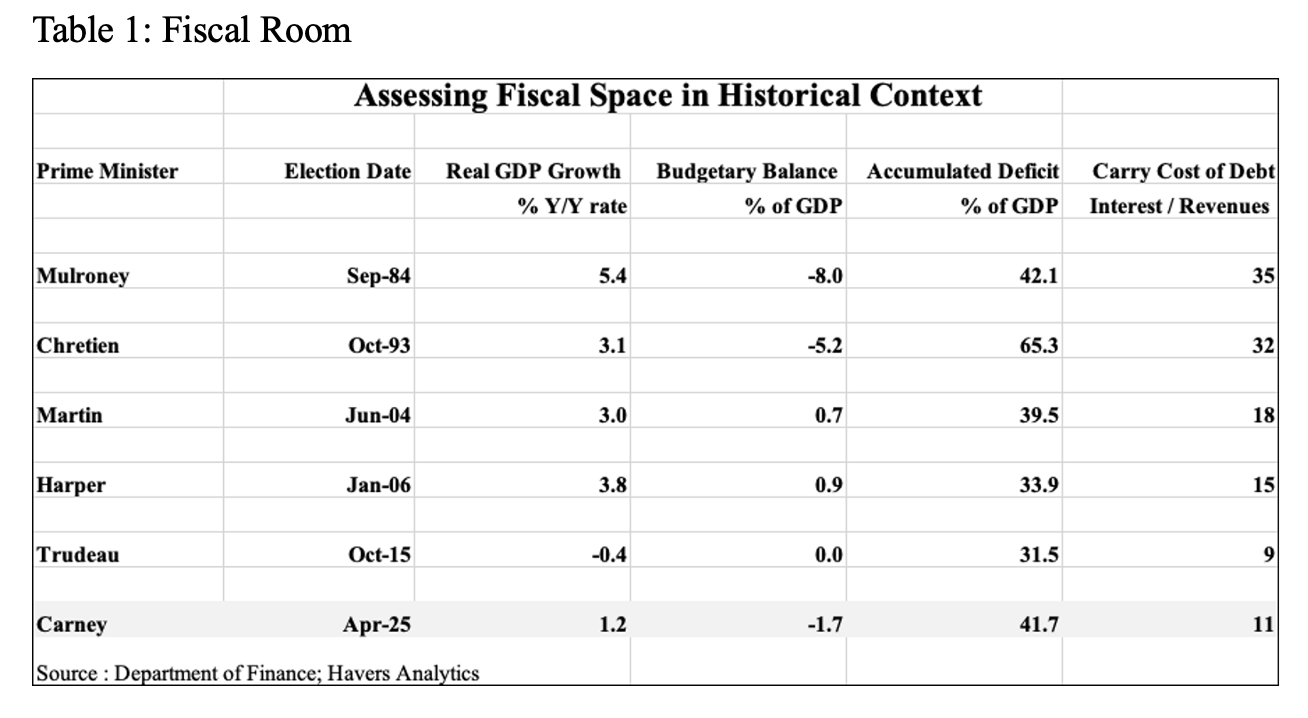

Table 1 lays out historic metrics on fiscal room over the past forty years. Bottom line, Canada has fiscal room to help finance the hinge moment.

Table 1 lays out historic metrics on fiscal room over the past forty years. Bottom line, Canada has fiscal room to help finance the hinge moment.

Relative to the past five Prime Ministers, Carney has been dealt a set of cards that are workable. The level of debt-to-GDP ratio is more akin to the Paul Martin era. It is more than 20 percentage points lower than numbers inherited by Jean Chrétien. Debt servicing costs are relatively low – only Trudeau inherited lower costs.

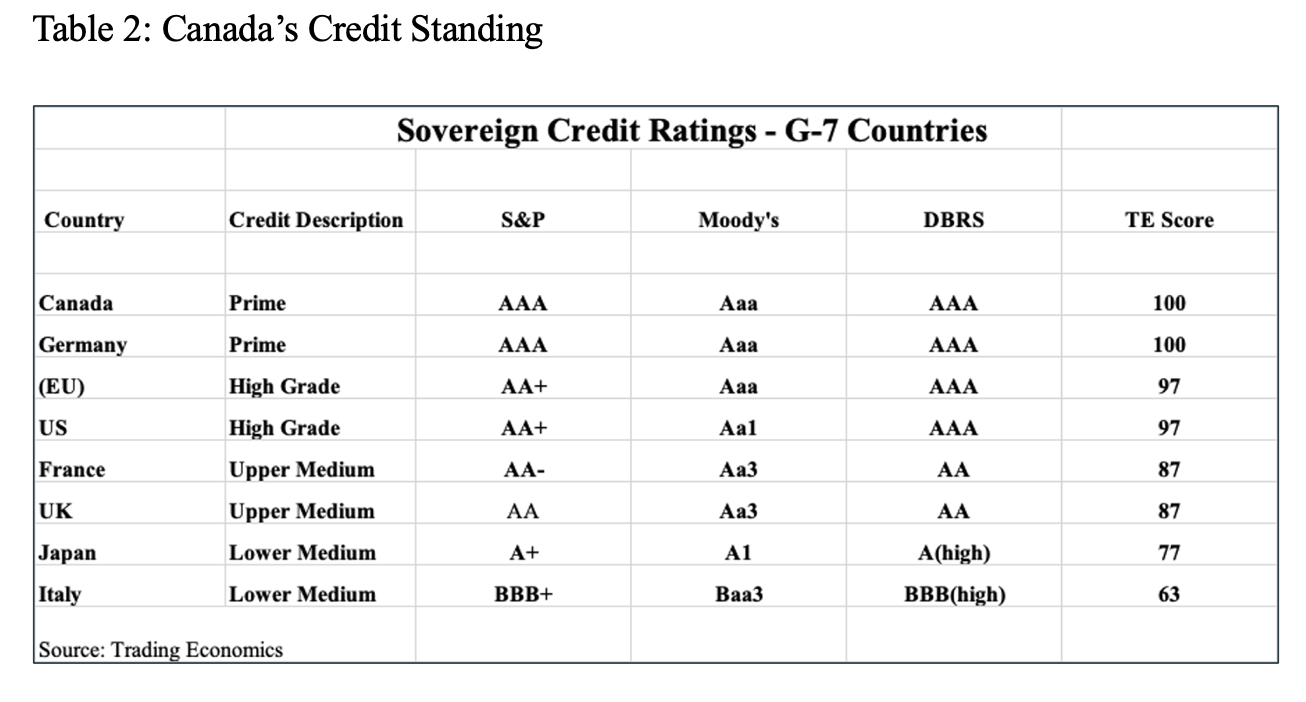

Along with Germany, Canada holds the strongest sovereign credit rating in the G7. The reality is that there is no fiscal crisis. No precipice.

When bond rating agencies look at Canada, they see strong fiscal institutions underscored by transparency and accountability. They see a fiscal track record that corrects imbalances – after the run-up in debt in the 1970s and 80s; after the 2008 financial crisis; after the 2020 global pandemic. They see strong financial assets backed by a good pension system. Canada has fiscal buffers.

The challenge for Prime Minister Carney is related to the hinge moment — the trajectory. The economy is weak and getting weaker. The deficit is widening, in part because of the weak economy. Short-term weakness because of the trade war and longer term because of low productivity growth. Interest costs are rising because of the large debt incurred to protect Canadian households and business during COVID and the uptick in interest rates.

Would Carney like to have had the fiscal-room metrics inherited by Harper and Trudeau? Yes. As the saying goes, “You can’t change the cards you are dealt, just the way you play your hand”.

IFSD illustrative estimates suggest the budgetary deficit with scaled implementation of the 2025 Liberal platform and NATO commitments could generate budgetary deficits in the $90 billion range in 2025-26 falling to $70 billion by the end of decade. As a percentage of GDP this would imply deficits in the 2.5 to 3%, falling to 1 to 1.5% by the end of the decade. This would likely be lower than the fiscal plans in most OECD countries. Increasing reallocation through spending review could bring into play the government’s platform commitment of an operating balance by 2028-29.

IFSD illustrative estimates suggest the budgetary deficit with scaled implementation of the 2025 Liberal platform and NATO commitments could generate budgetary deficits in the $90 billion range in 2025-26 falling to $70 billion by the end of decade. As a percentage of GDP this would imply deficits in the 2.5 to 3%, falling to 1 to 1.5% by the end of the decade. This would likely be lower than the fiscal plans in most OECD countries. Increasing reallocation through spending review could bring into play the government’s platform commitment of an operating balance by 2028-29.

It is anticipated that Budget 2025 will make the case with analysis that this is fiscally sustainable — a fiscal structure with a decline in the debt-to-GDP ratio over the long run.

PBO’s updated pre-budget fiscal outlook shows a positive and rising primary balance (program spending less revenues) over the medium term. This means that in the baseline context (before budget measures) the government is not deficit financing program spending (only debt interest). This is much different (better) than Canada’s fiscal situation in the 1980s, when we ran large primary deficits.

The government’s platform commitment is to balance the operating budget in 2028-29 (assuming no economic shocks). It has indicated that it will use deficit finance only for capital spending. It must operate with discipline. If this capital spending is used to generate productive assets and is scaled to ensure fiscal sustainability, it should be deemed fiscally responsible by Parliament, Canadians and credit rating agencies. Will it be sufficient to address Canada’s hinge moment? Canada’s crisis is not fiscal.

Kevin Page is the President of the Institute of Fiscal Studies and Democracy (IFSD) at the University of Ottawa, former Parliamentary Budget Officer and a Contributing Writer for Policy Magazine.

Adam Parwana and Hao Tian Shen are undergraduate economics students at the University of Ottawa.