Budget 2025: A Capital Investment Agenda

Shutterstock

Shutterstock

By Kevin Page

November 5, 2025

Finance Minister François-Philippe Champagne tabled Budget 2025 on November 4th. Given the spring election and the government’s commitment to change the financial cycle by tabling budgets in the fall, Parliament and Canadians are getting two budgets in one (2025 and 2026).

Margaret Atwood has said that the difficulty of governing from the centre is that you get attacked from both sides. The Liberal government will face a two-sided attack on the budget strategy and plan. In a minority Parliament, this creates risk to passage of the budget.

And, if this budget loses a confidence vote, it is possible we may get two elections before we chart and implement a collective path ahead in a world rocked by change, insecurity and uncertainty.

Two overarching questions should drive the budget debate.

One, is there a consensus on the economic and political challenges facing Canada? Is this a hinge moment requiring major policy shifts or a storm that can be navigated with existing equipment?

Two, is the country (and government) ready for a capital investment agenda? Major capital projects are expensive. They carry budgeting and implementation risks. Fiscal plans look different – there is separate planning and reporting on operating vs capital spending. There are highlights of cash vs accrual accounting. Wealth creation is driven by investments in infrastructure, machinery and equipment, technology and science. Redistribution, which is essential for social cohesion and fairness, is driven by progressive taxation and spending transfers.

Budget 2025 is the start of a capital investment agenda for Canada. It largely follows the policy script laid out in the Liberal election platform.

That policy script is driven by crisis — some would say a polycrisis: a rupture of Canada-US relations and a changing global trade order; heightened global insecurity with ongoing wars in Europe, the Middle East, and rising tensions between major powers; a revolution in innovation spurred by advancements in artificial intelligence, biotechnology and clean energy; ongoing and systemic domestic challenges from productivity to health care to climate change to inequality to relations with indigenous peoples.

My former boss, Privy Council Clerk Alex Himelfarb, used to say there is no risk-free risk. Military people have counselled that in dangerous environments, being risk-averse carries greater risk.

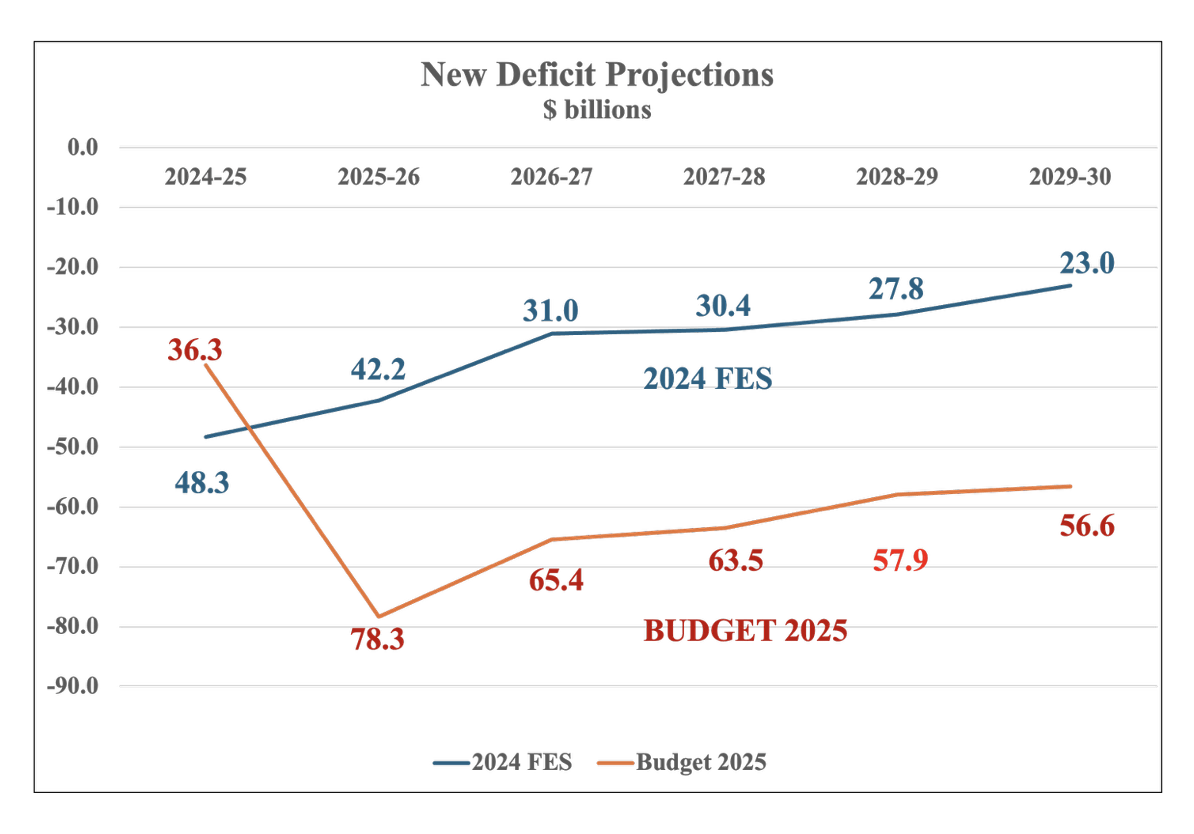

The government has tabled a large and relatively bold budget. The bottom lines are moving. More spending means more risk. Chart 1 highlights the higher deficit trajectory since the 2024 Fall Economic Statement (FES). Largely as anticipated by budget experts under a weaker economy and outlook, the projected budgetary deficits have doubled. The projected budgetary deficit for 2025-26 is now $78 billion – about 2.5 percent of GDP.

Chart 1

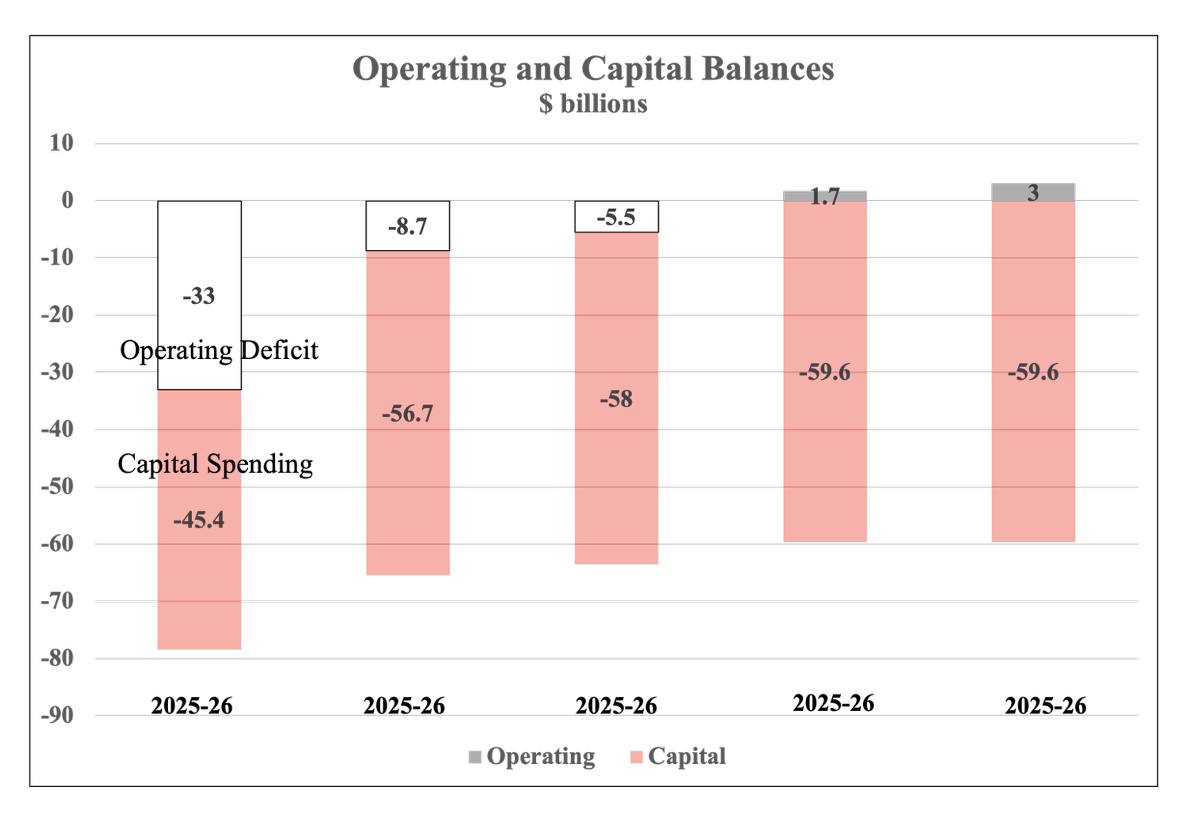

Chart 2 illustrates the fiscal plan for budgetary deficits. They are elevated. The decline is gradual. In 2028-29 the operating deficit is eliminated. Thereafter, ongoing projected deficits are for capital investment as defined in the budget. Currently, the projected deficit for 2028-29 is about $60 billion – about 1.5 percent of GDP. Parliamentarians, capital markets and Canadians (young and old) should hold the government accountable that under current economic planning assumptions, any debt accumulated is for capital investment.

Chart 2

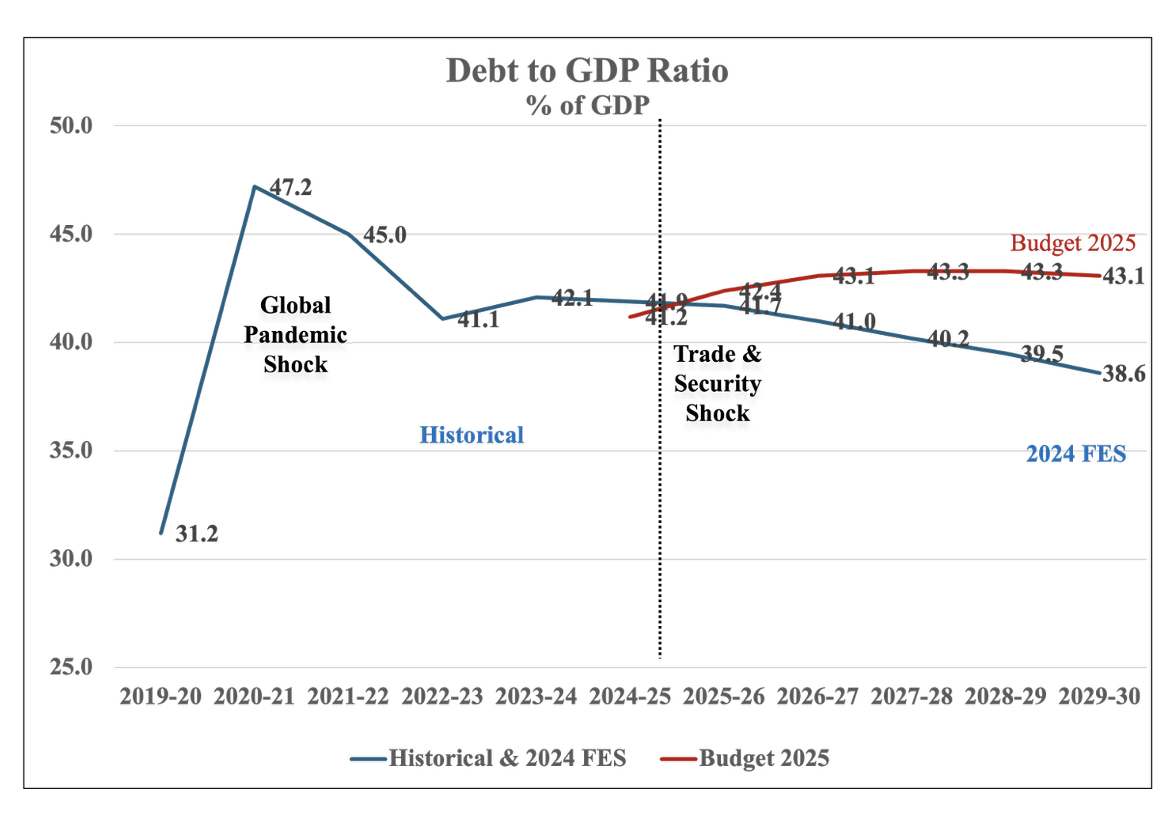

The debt-to-GDP ratio in Budget 2025 rises modestly and then flattens. Finance analysis indicates that the fiscal structure is sustainable over the long term. Fiscal room or buffers have been used to address the ongoing trade and security shock. Chart 3 shows that progress was being made in lowering the debt-to-GDP ratio since the global pandemic. Some of this progress is being reversed. There are no free lunches. Higher debt means higher interest costs.

Chart 3

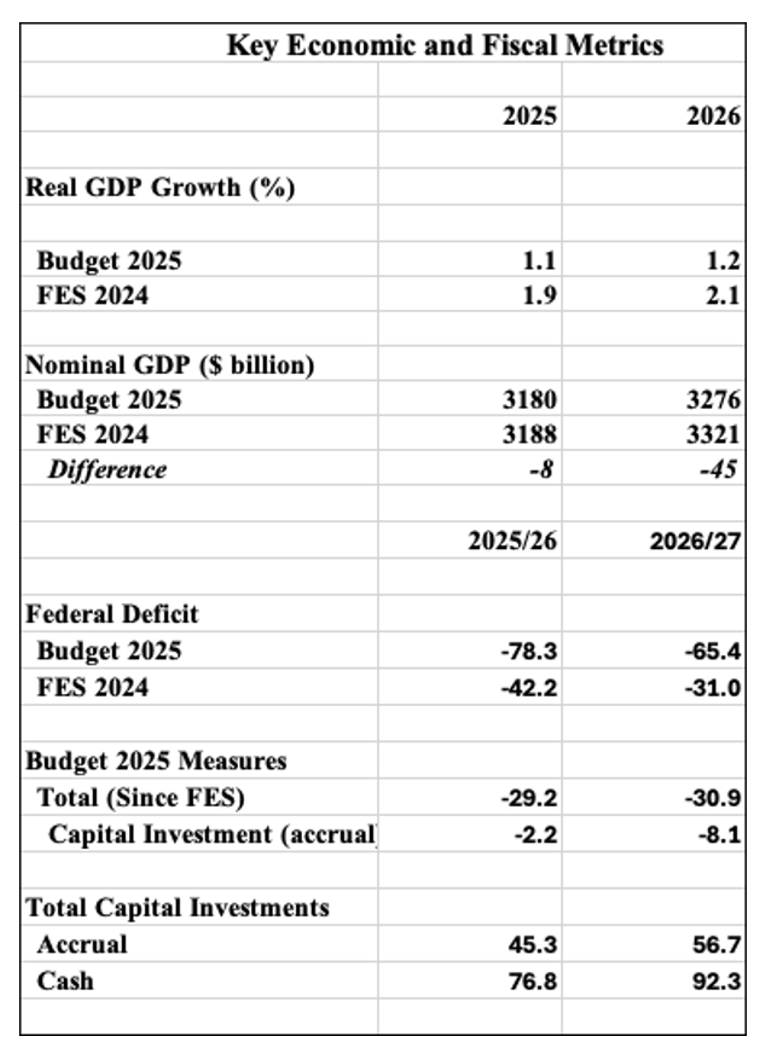

Budget 2025 is tabled in a period of significant economic weakness. Growth projections have been cut in half. Real GDP is expected to grow in the 1 percent range in 2025 and 2026 (Table 1). Weak growth means higher unemployment. In a $3.3 trillion economy, nominal GDP is down $45 billion in 2026. The higher projected deficits reflect a weaker economy and the government’s policy response. There are about $30 billion in new budget measures, primarily growth related, being injected into the economy each year. There is a significant projected increase in the level of capital investment (accrual and cash). If the budget and budget implementation acts get Parliamentary approval, close monitoring will be required on implementation and economic outcomes.

Budget 2025 is tabled in a period of significant economic weakness. Growth projections have been cut in half. Real GDP is expected to grow in the 1 percent range in 2025 and 2026 (Table 1). Weak growth means higher unemployment. In a $3.3 trillion economy, nominal GDP is down $45 billion in 2026. The higher projected deficits reflect a weaker economy and the government’s policy response. There are about $30 billion in new budget measures, primarily growth related, being injected into the economy each year. There is a significant projected increase in the level of capital investment (accrual and cash). If the budget and budget implementation acts get Parliamentary approval, close monitoring will be required on implementation and economic outcomes.

Table 1

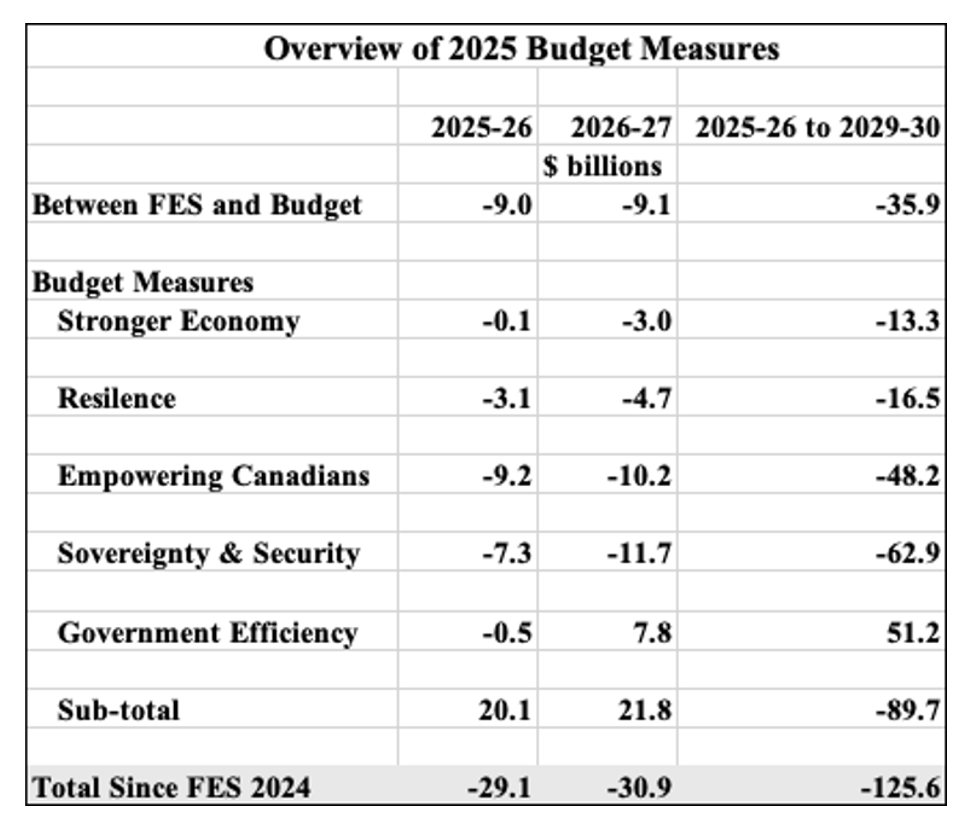

Table 2 outlines the large outlay of measures in Budget 2025. In total, new measures since the 2024 FES total about $126 billion over 5 years. This is a large fiscal injection relative to the size of the economy and past budgets. Is it sufficient in scale to merit a generational shift? Maybe not (yet). Clearly, the government was restrained in the size of the allocation by a host of factors, including generating offsetting savings in government efficiencies, and fiscal targets and rules with respect to achieving an operating balance in 2028-29 and showing a declining budgetary deficit relative to GDP. The base and magnitude of government efficiencies currently being planned is consistent with the Liberal platform.

Table 2

In early positioning on this budget, the Conservatives want a smaller deficit, a bigger tax cut, and more help on affordability. The NDP will find it hard to support a budget with sizeable reductions to the public service (i.e., government efficiencies). The Green Party will raise concerns about the government backing away from their climate agenda. The Bloc want more transfers to seniors and the province for health care.

The beauty of a democracy is that we have debates and compromises.

Can we find consensus on the economic and fiscal challenges facing Canada? Are we facing a crisis?

Is the country ready for a capital investment agenda?

Kevin Page is the President of the Institute of Fiscal Studies and Democracy (IFSD) at the University of Ottawa, former Parliamentary Budget Officer and a Contributing Writer for Policy Magazine.