The 2026 Spring Economic Update: Fiscal Dividends Get Allocated

By Kevin Page

April 29, 2026

Finance Minister François-Philippe Champagne tabled the Spring Economic Update (SEU) in Parliament on April 28, 2026 – six months after the fall budget and on the one-year anniversary of the federal election; a symmetry between the political and financial cycles that underscored Prime Minister Mark Carney’s economic credentials.

In Tuesday’s SEU, the Carney government made its best case to maintain and bolster confidence in the Canada Strong plan. A resilient economy in the face of high economic and political uncertainty and an oil price shock provided the government some fiscal room to address current policy pressures and maintain its fiscal planning framework.

The policy decisions in the 2026 SEU highlight that there are two distinct policy horizons in the Canada Strong plan: a short-term horizon dedicated to promoting economic stability with fiscal policy, including support for affordability issues related to food, energy and housing prices; and a longer-term horizon focused on capital formation to boost productivity, support trade diversification, and strengthen national defence in line with NATO commitments.

Did the government live up to the slogan “spend less, invest more”? No. In turbulent times with a relatively weak economic outlook, the government choose to spend the fiscal dividend on current operations/consumption-type spending, not capital investments, not deficit reduction.

Follow the Money

There are many dimensions and perspectives on financial documents. Numbers can help develop a narrative.

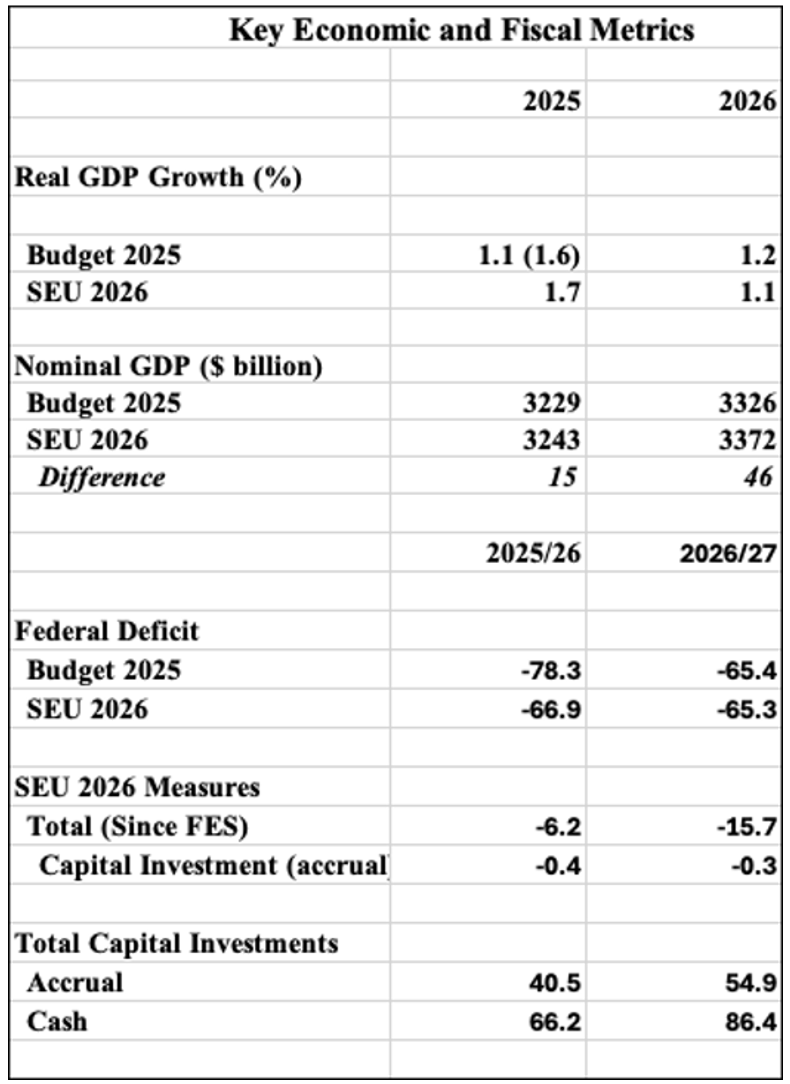

The average private sector economic forecast indicates the size of the (current dollar) economy got bigger in the Update relative to November 2025 Budget. Nominal GDP is up $46 billion in 2026 thanks to higher prices, particularly oil prices. A bigger (more inflated) economy means more revenues.

Real GDP, by contrast, is forecasted to grow only 1.1% in 2026, after growing 1.7% in 2025 – that’s weak. It means the economy is performing well below its potential.

Chart 1: Metrics

Note: Statistics Canada GDP revisions increased the growth rate in 2025 relative to the November budget forecast

The average private sector forecast for oil prices in 2026 is $73 US per barrel (West Texas). It is higher than the November planning number but well below current spot and future prices. This could mean that there may be more revenue relief in the planning framework for 2026. Higher oil prices are typically a net positive for the federal treasury.

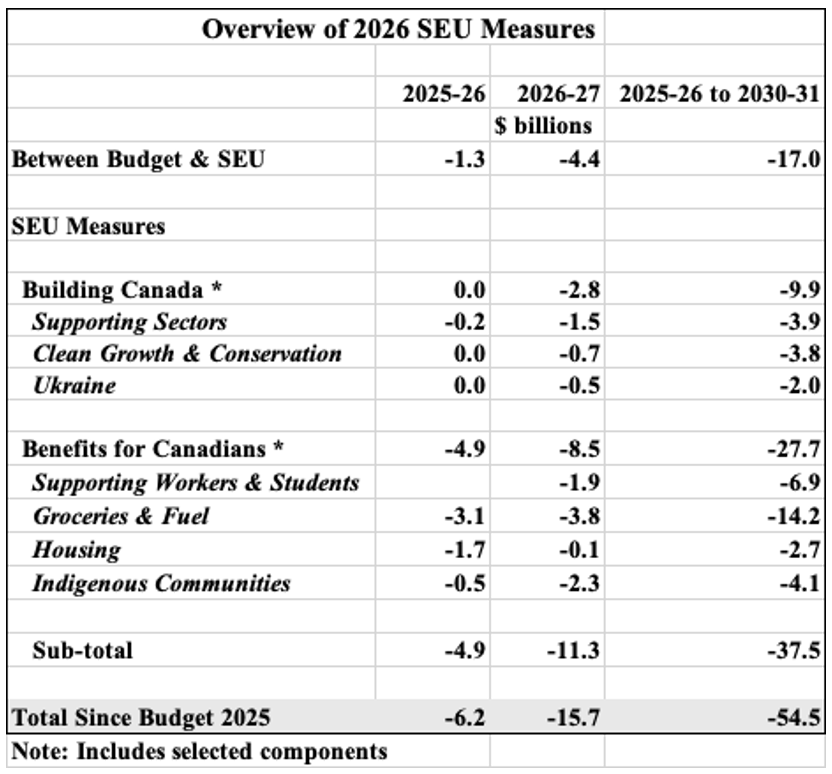

Economic and fiscal developments since the November 2025 Budget generate about $60 billion in fiscal room over the six-year planning period. It is a modest amount (i.e., Canada is a $3.3 trillion economy).

What does the federal government do with the fiscal dividend? It spends more than 90% ($54.5 billion) over the fiscal planning period.

The 2026 SEU projected a budgetary deficit for 2025/26 well below the November estimate ($67 billion versus $78 billion). This reflected both higher-than-expected revenues and government spending (capital and operating) that did not get out the door. Thereafter, the deficit track remains virtually identical.

Budgetary deficits are in the $65 billion range over the next few years (about 2% of GDP and declining modestly). As the government notes, this is a modest deficit relative to many OECD countries (and about one third the relative size of the US budgetary deficit).

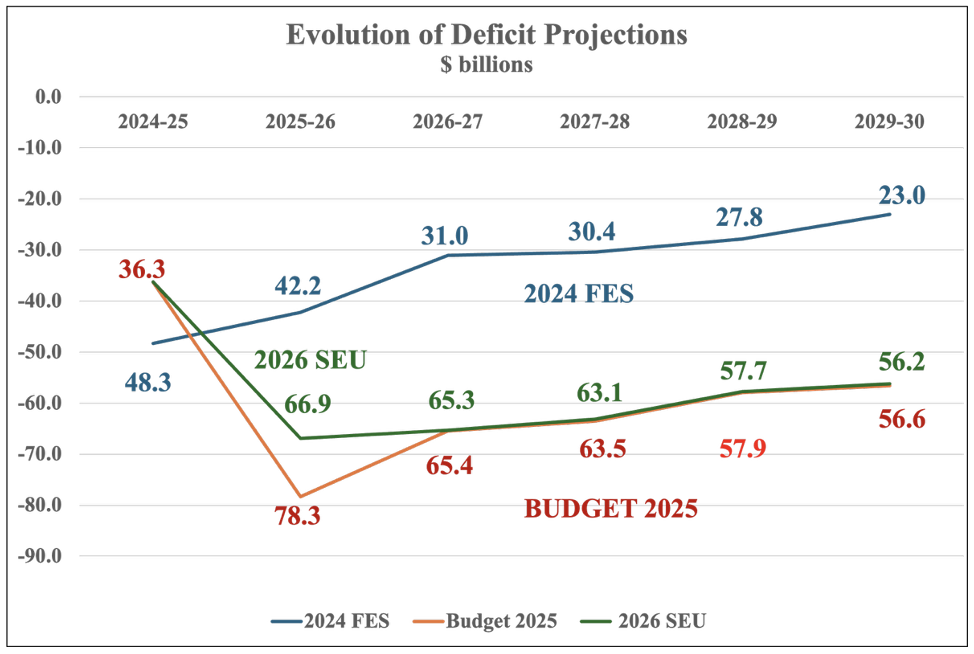

Chart 2: Budgetary Deficits

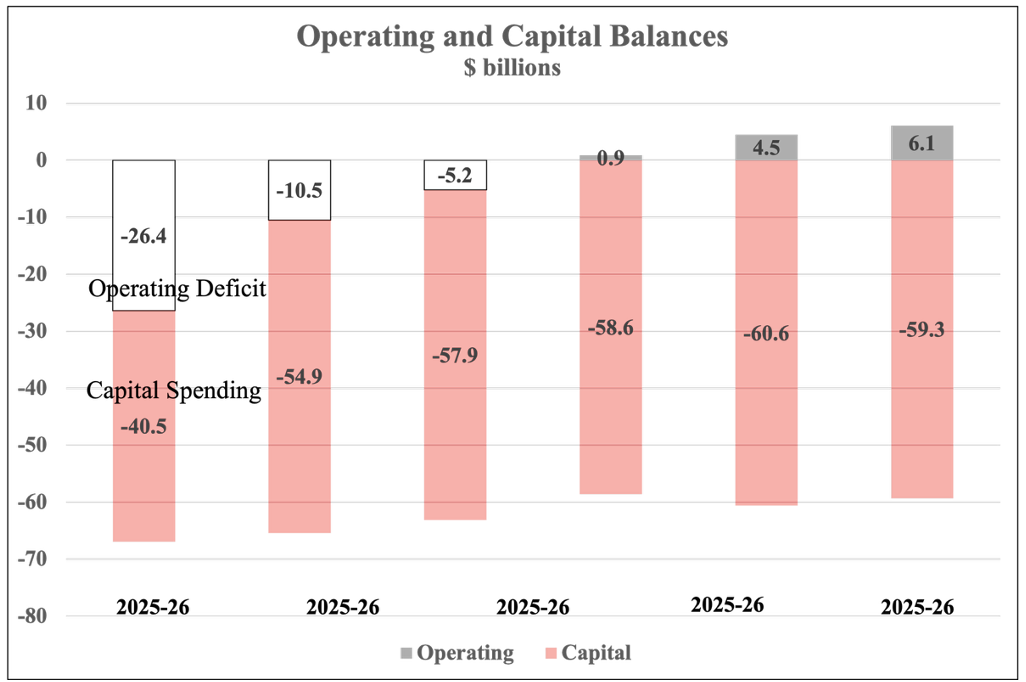

The government maintains its primary fiscal objective of balancing the operating budget in 2028-29. Thereafter, budgetary deficits are supposed to be only for capital investments.

Chart 3: Operating vs Capital

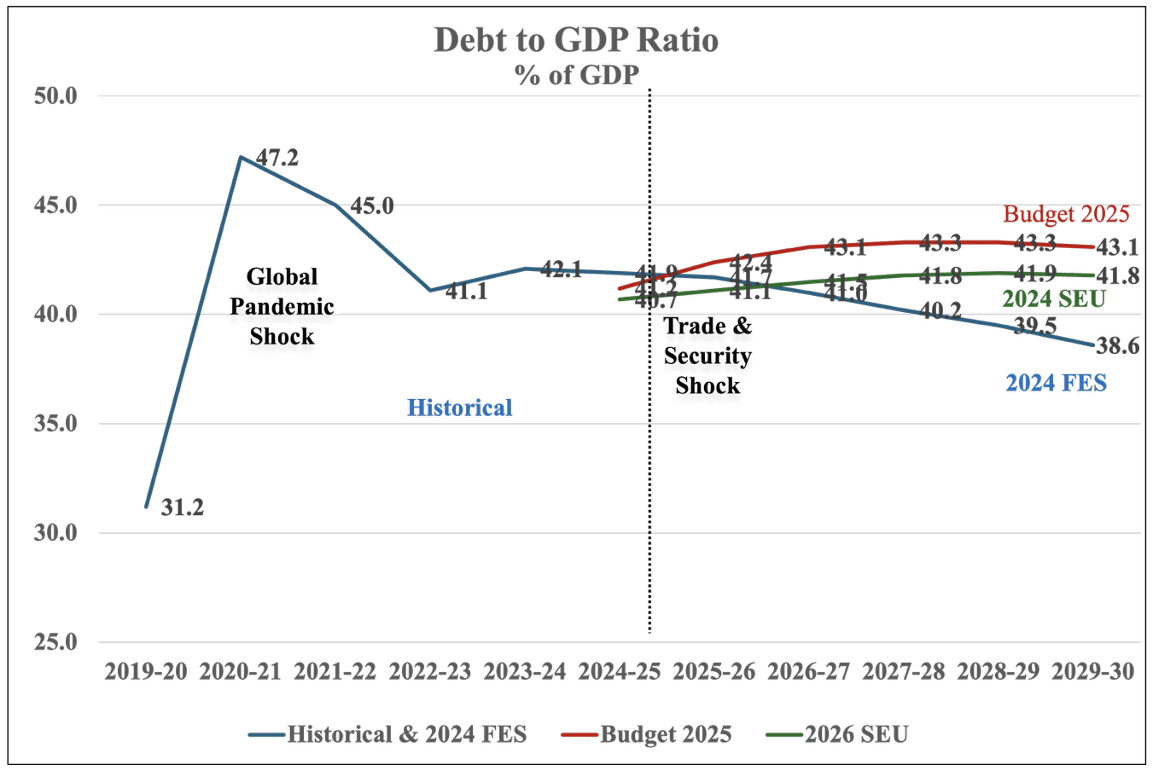

The government’s debt-to-GDP ratio remains relatively flat over the planning horizon but is lower than projected in the November 2025 Budget. That flat profile reflects a number of factors – a weak economy over the short term; and higher spending over the medium term, notably for national defence that is deficit-financed.

Chart 4: Debt-to-GDP

A significant proportion of the total new measures highlighted in the 2026 SEU is allocated over the short term (40% or $21.9 out of $54.5 billion). This is generally good from a fiscal stabilization perspective because it is targeted when the economy is operating well below potential. Less than $1 billion per year of the new spending is related to capital investments. This SEU is spending more but not investing more.

There are effectively three types of new spending. Spending since the November 2025 Budget (but before the Update) could be categorized largely as program integrity spending. These are existing programs (e.g., air transport security, the Jordan’s Principle program for First Nations children, employee benefits, etc.) that need additional resources to address service-level pressures. They represent $17 billion out of the total $54.5 billion (about 30%).

About $10 billion over the planning period is allocated to what the Government calls in Chapter 1 Building Canada: All for Canada. It is a hodgepodge of measures combined to support strategic sectors through adjustment, from the government’s automotive strategy to Canada’s support for international climate finance to fulfilling commitments to NATO and Ukraine.

The third type of new spending is outlined in Chapter 2: Benefitting Canadians: A Canada for All. It is the largest bucket at $27.7 billion or 50% of the new outlays since the November 2025 Budget. It includes key measures to address affordability – groceries, fuel, housing, and supports for Indigenous communities. There are signature initiatives to support the skilled trades and the extension of aids to help students. There are also initiatives to support access to disability benefits that do not draw significant resources from the treasury but could be very helpful for people in need. A reduction in CPP contribution rates was announced with the Update although it will not directly impact the federal bottom line.

Chart 5: Measures

The pre-update announcement of the Canada Strong Fund, Canada’s first national sovereign wealth fund, was in the update. However, additional details on the fund were not provided, nor was there a transparent accounting of the $25 billion deficit- financed cash that will help kickstart the fund. The creation of the fund is considered an important development in the Canada Strong Plan, with the objective of increasing foreign direct investment in Canada. More information and consultation on the fund are expected in advance of a planned international conference on investment in Canada later this fall.

A More Traditional Mid-Year Update

In many respects, the 2026 SEU resembles a more traditional economic update, with a greater focus on the evolving economic outlook and its impact on the government’s fiscal strategy, plan and outlook. It is a much smaller and more focused document (170 pages versus a 400-page Budget). It provided important information on key planning assumptions (e.g. oil prices) with perspectives on risks and scenarios. It provided important transparency on program integrity initiatives (i.e., changes in spending between the Budget and SEU).

Needs and Opportunities for Improvement

There is a very large transparency gap in the planning outlook. The government’s commitment to work towards the new NATO defence targets is not shown in the tables on program spending. Canadians, notably parliamentarians, need to see the planning baselines for the Department of National Defence and what it means for NATO targets.

Within the post-financial crash two-year fiscal stimulus plan of the Harper government in 2009-10, parliamentarians requested and received operational updates on all measures. Given the scope and scale of the Canada Strong plan, Canadians and parliamentarians would benefit greatly from an operational planning document from the Carney government that shows results against all its commitments.

Kevin Page is the President of the Institute of Fiscal Studies and Democracy (IFSD) at the University of Ottawa, former Parliamentary Budget Officer and a Contributing Writer for Policy Magazine.