The Spring Economic Update: Canada Strong, Deficits Long

April 29, 2026

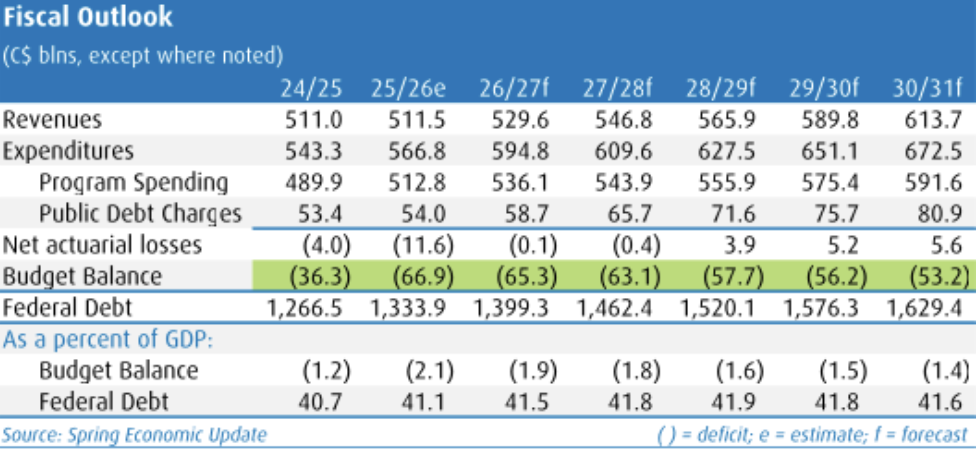

Ottawa is projecting a $65.3 billion deficit (1.9% of GDP) for FY26/27 in the Spring Economic Update, little changed from the $65.4 billion forecast in the original budget plan (recall that was tabled in November). A broadly stronger revenue environment has helped, but that improvement was fully soaked up by new program announcements.

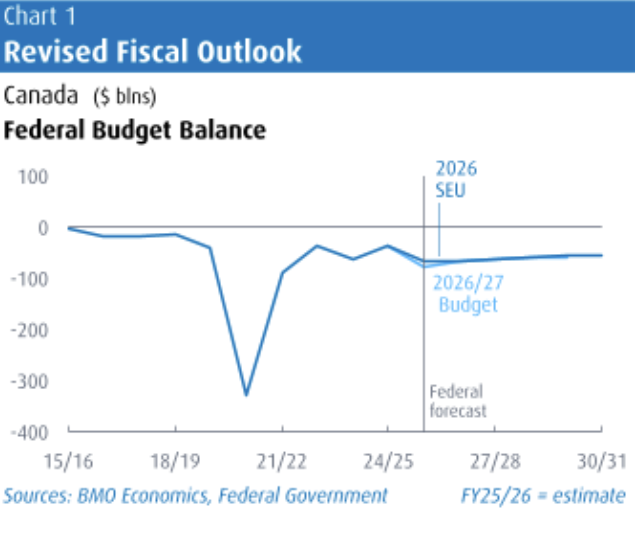

The deficit for FY25/26 (the fiscal year that just ended in March) did come in better than expected at $66.9 billion, down from the $78.3 billion assumed in the fall. Deficits track very modestly lower through the forecast horizon, but remain well in the red at $56.2 billion by FY29/30. All in, the five-year cumulative improvement in the bottom line runs at $12.5 billion, confirming the better news that Ottawa was floating in recent days.

Meantime, the debt-to-GDP ratio rises this fiscal year, by 0.4 ppts to 41.5%. But, the level is tracking notably lower than the 43.1% penciled into the budget plan, mainly on the back of upwardly-revised Canadian nominal GDP. The ratio edges up gradually for two more years before finishing little changed at 41.6% in FY30/31.

The improvement to FY25/26 comes as the result of very positive economic and fiscal developments, offset partly by new spending/tax measures—perhaps the government just couldn’t get the money out the door fast enough. But that is not looking like an issue for FY26/27, where $15.7 billion in positive economic and fiscal developments have been fully offset by new measures. Among those are the temporary removal of the excise tax on gasoline; removal of the GST on new homes for all buyers; expansion of the GST/HST credit under the Canada Groceries and Essentials Benefit banner.

Income taxes drove most of the underlying improvement to the tune of $6.8 billion in FY25/26 and $10.0 billion in FY26/27. Revised timing for spending in some areas such as Clean Economy tax credits and EV supports also pulled down baseline program spending.

Meantime, debt service costs are tracking somewhat lower than expected with the Bank of Canada firmly on hold, and despite the recent backup in bond yields. Ottawa now expects debt service costs to rise to $58.7 billion this year from $54.0 billion. That will come in at just over 11% of revenues this year, and will continue to drift higher on this basis through the forecast horizon.

Major New Measures

New measures announced since the fall budget come in at $15.7 billion this fiscal year, and average $8.2 billion per year over the following four years. Ottawa continues its trend of adding significant stimulus into an economy that has held up relatively well, especially given the headwinds of the trade shock.

Most big ticket measures, including the cut to the gas tax (cost: $2.4 billion this fiscal year) and the Groceries and Essentials Benefit ($1.4 billion) were previously announced.

There were few new details on the Canada Strong Fund. This update confirms a $25 billion initial investment by Ottawa through government funding (i.e., borrowing), retail investment and asset sales. The cost doesn’t flow through the operating statement and to the reported deficit. Suffice it to say this not the “sovereign wealth fund” that many would think of, such as those that save a dedicated portion of certain revenues/surpluses for future generations. Rather, it looks like another borrowing vehicle to tap to fund priority projects. Further details are still forthcoming.

One of the biggest new items is an initiative to train and hire 80-to-100k workers to the skilled trades by 2030-31. The measure is expected to cost $0.7 billion this fiscal year and roughly $1.2 billion per year thereafter, after accounting for existing funding and a small boost to revenues. This will be through wage subsidies, program tuition grants and cash bonuses for completion of training.

Meantime, affordability challenges remain in focus. Here, the flagship new measure is a cut to the CPP contribution rate from 9.9% to 9.5%, starting on January 1, 2027. According to the latest estimates, the lower rate would still be above the minimum required to keep the plan sustainable for the next 75 years. And, importantly, the CPP is fully self-funded, meaning this measure doesn’t come with a cost for the government—a rare win-win-win for affordability, fiscal finances, and program sustainability.

A few other tax measures come with smaller price tags, including tweaks to make the Disability Tax Credit easier to access, and making permanent the temporary tax exemption of capital gains on the sale of a business to an employee ownership trust.

On the environmental side, and following last year’s MOU with Alberta, the government is expanding eligibility for the Carbon Capture, Utilization, and Storage investment tax credit to enhanced oil recovery. The credit is set to 30% for direct air capture equipment, 25% on other capture equipment, and 18.75% for transportation and storage/use equipment, as long as the captured carbon dioxide is stored permanently. The measure is expected to raise $0.4 bln in revenues over four years, starting in FY27/28.

Economic Outlook

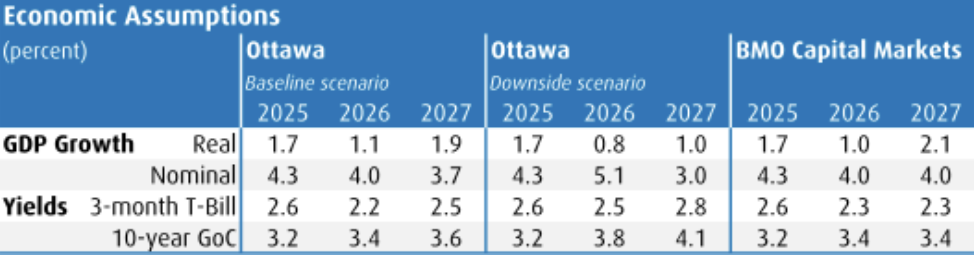

Ottawa is basing this fiscal update on a consensus survey from March, taken as the conflict in Iran was heating up. The outlook assumes 1.1% real GDP growth this year, followed by 1.9% growth in 2027. Nominal growth is pegged at 4.0% this year and 3.7% in 2027. BMO Economics currently sees 1.0% real GDP growth in 2026, picking up to 2.1% in 2027, with nominal growth running at 4.0% in both years. Uncertainty still abounds on multiple fronts including the Canada-U.S. trade relationship, and in global energy markets. We are largely assuming status quo on Canada-U.S. trade unless material progress can be made leading into the CUSMA renewal period, and we view the impact of higher oil prices as very mixed for Canada—great for producing regions, but a meaningful drag in others. All told, the Bank of Canada looks to be on hold through 2026, which is consistent with Ottawa’s current interest rate assumptions.

Debt Management Strategy Update

The Debt Management Strategy Update leaves total gross bond issuance unchanged at $298 billion for FY26/27. Benchmark sizes are also unchanged, while bill issuance will be trimmed by $23 billion, to $268 billion.

The Bottom Line

The headline-grabbing new measures announced recently, and in this document, have rolled more fiscal stimulus out onto the economy. They have also soaked up a better underlying fiscal position, leaving the deficit little changed for FY26/27 and beyond.

Robert Kavcic is Senior Economist and Director Economics for BMO Capital Markets.