Donald Trump’s Choice for Central Banker

Federal Reserve chair nominee Kevin Warsh/AP

Federal Reserve chair nominee Kevin Warsh/AP

By Kevin Page and Djeima Ramos

February 5, 2026

The nomination of Kevin Warsh as the next Federal Reserve chair by President Donald Trump will continue to draw market and political attention in the days ahead. The stakes are high.

After the controversies of the past year, will the Fed be able to protect its independence? If not, what might this mean for market (in)stability? For Canada?

Fiscal and monetary policymakers have been riding a roller coaster for nearly two decades, from the 2008 global financial crisis to the 2020 COVID-19 pandemic to the post-pandemic effort to rein in inflation. That roller coaster has continued with the advent of protectionist U.S. trade policy and demands for higher military spending in a less secure world.

Why has the nomination of Kevin Warsh drawn such significant media and market attention?

- The U.S. dollar is the currency of choice for global trade and financial contracts. U.S. treasuries are the world’s largest bond market. Many countries, including Canada, are pressured to follow Fed policy or risk capital and currency shocks. Geopolitical ructions notwithstanding, the Fed remains the world’s most important central bank.

- After a year spent as a target of Donald Trump’s ire, Fed Chair Jerome Powell’s term expires in May. Powell is highly regarded among experts for his competence and has skilfully defended the independence of the Fed. But the controversy has drawn disproportionate attention to the question of who will succeed him.

- President Trump is widely regarded to have undermined U.S. institutions by usurping their roles (e.g., Congress on the setting of tariffs). He has argued that U.S. should have the lowest interest rates in the world.

Independence is a core principle of modern central banking. International research underpins its importance with respect to inflation, currency, financial stability and credibility. We want interest rates set by experts mindful of data and long-term implications, not short-term political pressures to drive rates lower and create an inflationary problem.

The resignation of Bank of Canada Governor James Coyne in 1961 over a dispute of policy with the Diefenbaker government was an important domestic and international moment in the movement towards central bank independence. It resulted in fundamental changes to the Bank of Canada Act involving the strengthening and clarification of independence and on governance, policy, and tenure.

Central bankers in Canada and the US have been on the policy hot seat.

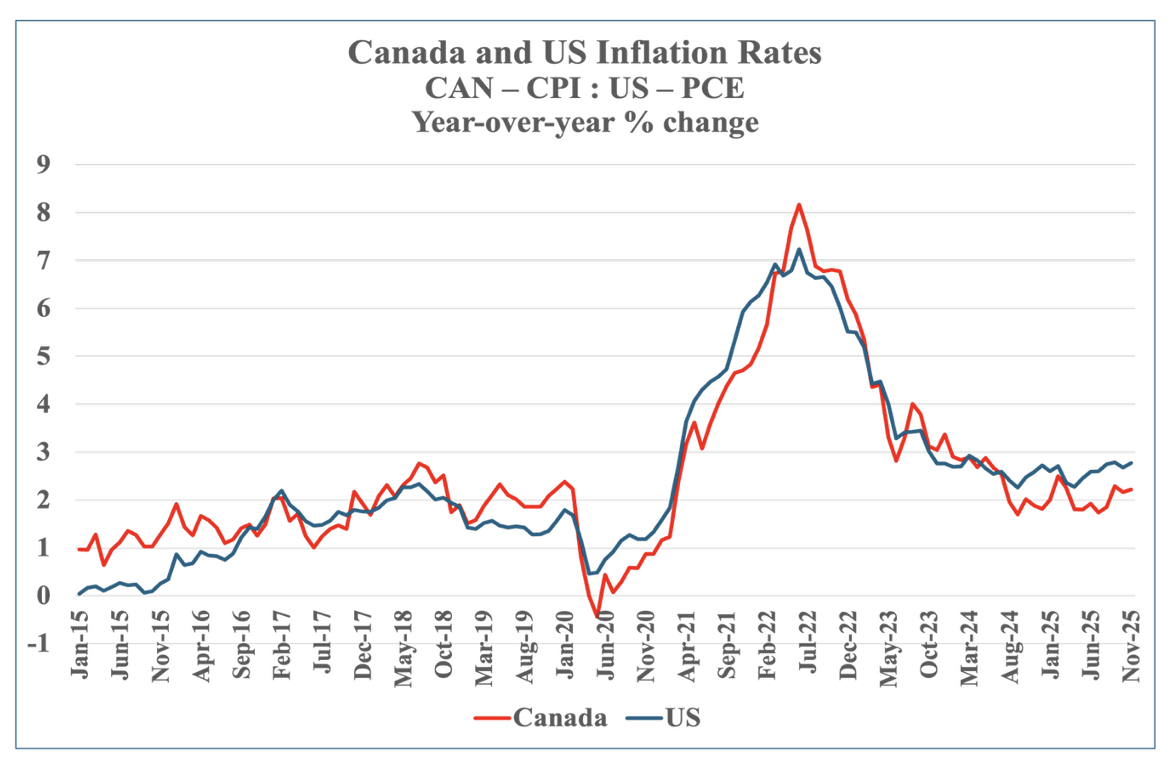

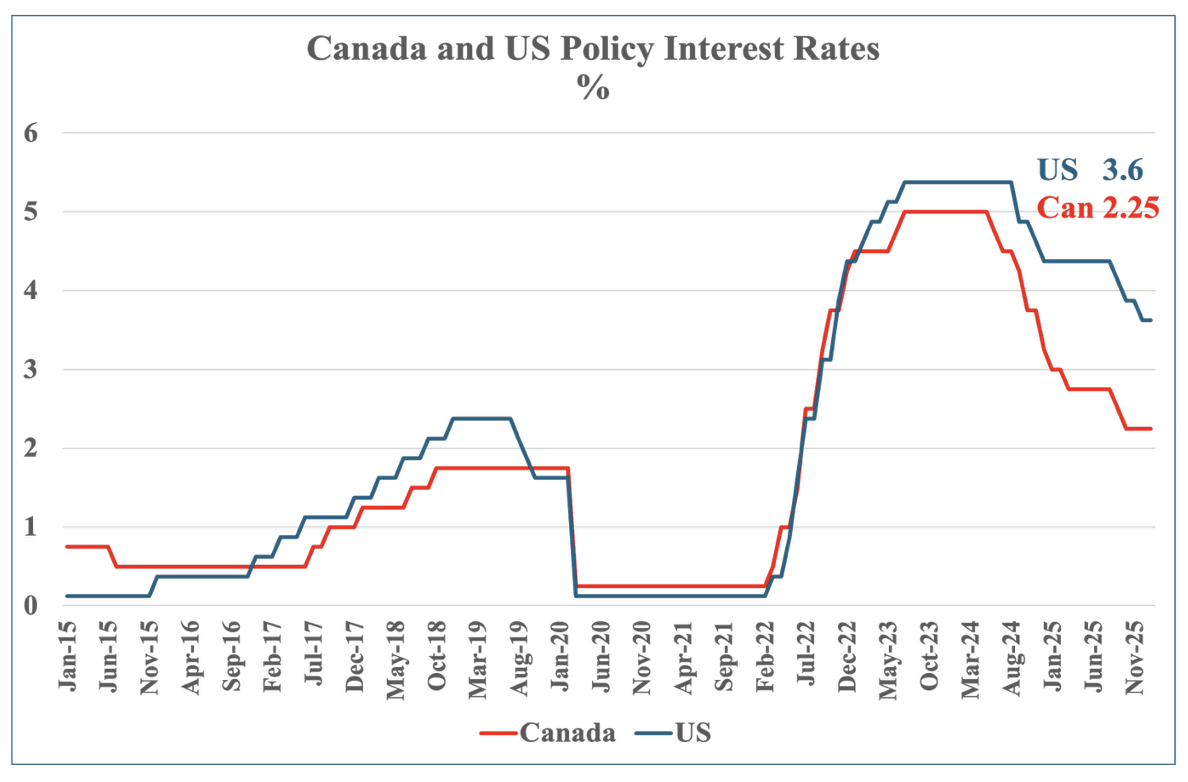

Bank of Canada Governor Tiff Macklem took serious political heat and scrutiny during the rise of inflation and interest rates (Charts 1 and 2) in the post-COVID recovery. During the Conservative leadership campaign in 2022, Pierre Poilievre threatened to dismiss Macklem if he became Prime Minister. It was an unusual threat, which the (now) leader of the Opposition has not raised since.

In response to the political pressure, Macklem responded at a press conference that it is in the difficult times requiring tough decisions (with a view to the long term) when you see the value of independence.

Chart 1

Source: Havers Analytics

Source: Havers Analytics

Note: PCE represents the chained price index for personal consumption expenditures. It is the key inflation indicator used by the US Federal Reserve

Chart 2

Source: Havers Analytics

Source: Havers Analytics

Since President Trump took office for the second time in January 2025, his pressure on Powell has been relentless. He has openly threatened to dismiss the chairman. He has sought to remove Fed Governor Lisa Cook (the Supreme Court intervened). The U.S. Department of Justice has issued subpoenas against the bank and the chairman. The consequence has been financial uncertainty, market instability and likely higher bond yields.

Policy and political pressures on central bankers are not going away. In Canada, the latest Abacus poll (January 2026) has the cost of living as the top priority for citizens; the economy is number two, and housing is right behind.

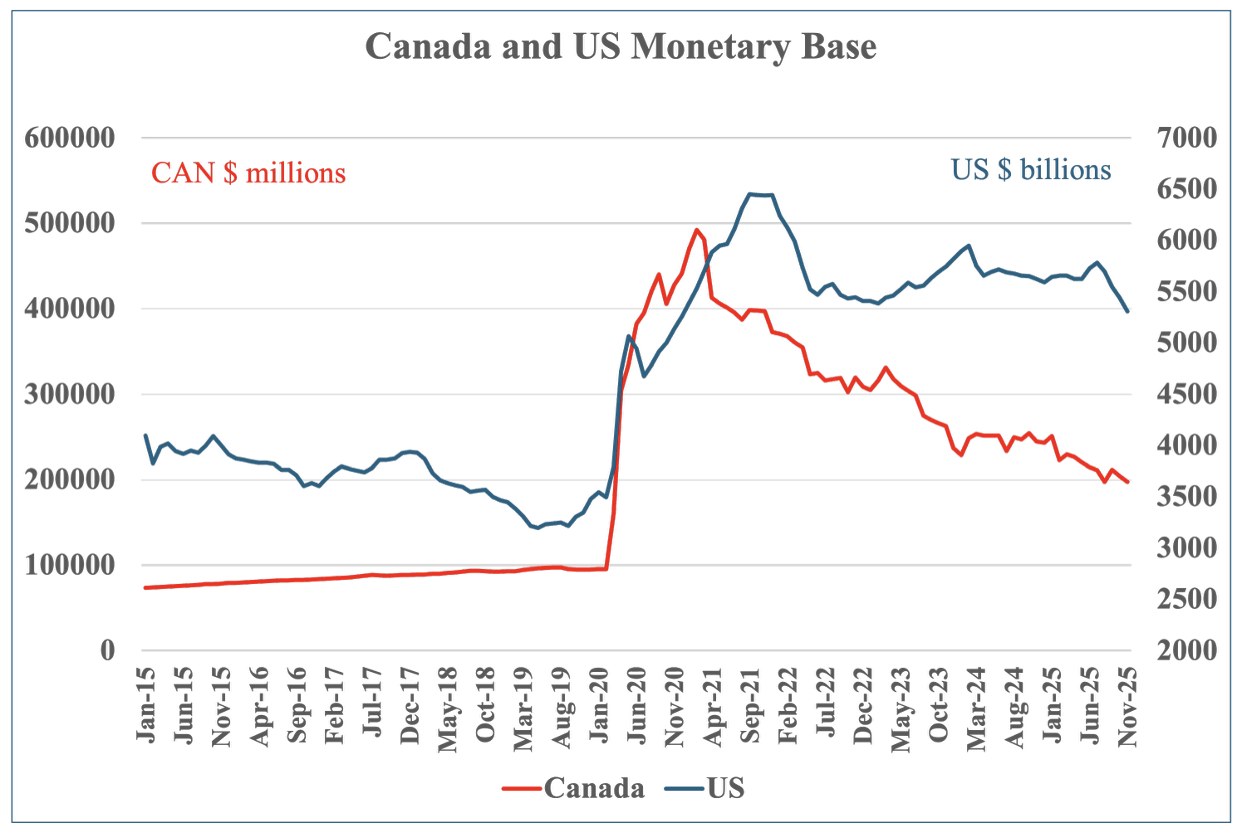

Monetary policies of Canada and the U.S. have largely followed similar paths through the pandemic period. Policy rates increased dramatically following the upswing in inflation rates, peaked and have declined (Charts 1 and 2). The monetary base (currency in circulation plus commercial bank reserves held in the central bank) rose dramatically and then trended down (Chart 3).

Chart 3

Source: Havers Analytics

Source: Havers Analytics

Note: the monetary base is a measure of money supply – notes in circulation and commercial bank reserves held at the central bank

Monetary policy in Canada could be described as in a neutral/holding pattern — policy rates (at 2.25 percent) have steadied near its trend rate and inflation is in the target zone of 1 to 3 per cent. It is a cautious pause in a period of uncertainty.

U.S. policy is in a more restrictive stance. The policy rate is much higher (at 3.6 percent) than Canada’s, reflecting higher inflation pressure stemming from government trade and fiscal policies and very strong investment in AI. The U.S. has made less progress in reducing its monetary base after the COVID build up.

President Trump promised progress on affordability. Interest rates are a key lever. While oil prices have eased, U.S. trade (tariff) and fiscal (deficit) policies have been inflationary.

So, everyone wants to know: How will the next Federal Reserve chairman stand up to power?

Comparison of processes for appointment of central bankers gives Canada an edge on the perception of independence.

In the U.S., the process is political in nature and design. The underlying principle is political accountability and public scrutiny. The president nominates and the Senate confirms. There are public hearings. The markets play a key role in keeping the president in check. This explains in part the testing of a candidate’s nomination in the public before official nomination.

In Canada, the process is technocratic. The underlying principle is institutional independence. The bank’s board selects the candidate. The executive (cabinet) approval is considered a formality. There are no parliamentary hearings. The process is designed to keep politics at arms-length. Tenure is set at 7 years (versus 4 for the U.S.).

It can be argued that bank governance structure gives more power to the U.S. Fed chair in influencing rate setting, although neither governor can act alone. In the U.S., the body that sets policy rates (Federal Open Market Committee) has 12 voting members. The chairman sets the agenda and guides the discussion. In Canada, the council (governor and deputies) operates via consensus. The governor does not have a vote, although remains the spokesperson and leader.

What do we know about Kevin Warsh?

He has credentials. He served as a Federal Reserve Governor (2006-2011), appointed by President Bush. He has Wall Steet experience (Morgan Stanley). He has a law degree from Harvard and has studied economics at MIT. He is a distinguished fellow at Stanford University’s Hoover Institution and sits on a panel of advisors for the Congressional Budget Office (CBO).

Market reaction to Warsh’s nomination was mixed. Mild volatility in stocks. Modest increases in bond yields and the dollar suggesting expectations that rate policy may remain tighter than with another candidate.

Analysts are cautious. Their assumption is that Warsh is more aligned to President Trump’s preferences for lower rates.

In an interview with NBC news on February 4, 2026, President Trump said that “in theory” the Federal Reserve is independent. He argued that the Fed should follow his directives because he knows the economy “better than almost anybody” — a comment that echoes other statements from this president in which ignorance is used to rationalize otherwise highly implausible, norm-breaking policy choices.

Hypothetically, should a new Fed chair result in significant (unexpected) reductions in the U.S. policy rate, we could be facing a shock to the confidence in the U.S. financial system.

How will equity markets react? They were sensitive to President Trump’s executive orders on tariffs on so-called Liberation Day (April 2, 2025). When Trump reversed course and lowered tariffs in response to market volatility (i.e. the so called ‘TACO’ reversal…Trump always chickens out), markets recovered quickly. Will markets remain the key back stop for President Trump’s ambitions on interest rates?

Significantly lower interest rates would provide short-term stimulus to the U.S., something desired by the President to bolster weak public polling heading into the U.S. fall mid-term elections. Many independent analysts will argue that the short-term economic benefits from easier borrowing will be offset by higher inflation over the medium term.

Because the U.S. dollar dominates global finance, the impacts on other countries will be quick. A lower U.S. dollar following rate reductions will drive up commodity prices (priced in U.S. dollars). Some of this inflation will spill over into other countries. A relative strengthening in the Canadian dollar will help Canadians with the cost of imports, but it will hurt exporters.

In the meantime, on this side of the border, Governor Macklem’s term expires in June 2027.

Policy Contributing Writer Kevin Page is president of the Institute of Fiscal Studies and Democracy (IFSD) at the University of Ottawa and former Parliamentary Budget Officer.

Djeima Ramos is a fourth-year undergraduate economics student at the University of Ottawa.