Forget TACO, Think SUSHI

By Douglas Porter

July 18, 2025

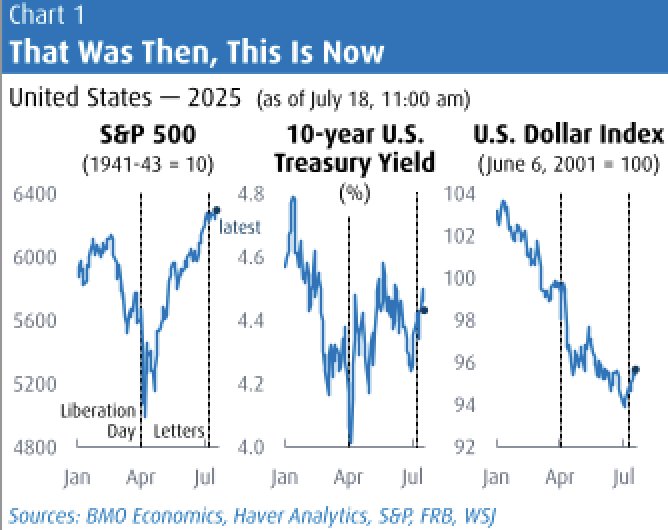

Stocks Usually Stop Having Interest (SUSHI) in issues or geopolitical events that don’t directly impact earnings or don’t have an immediate bearing on the interest rate outlook. And it is becoming increasingly clear that the market is losing interest, or at least is much less sensitive, to new developments on the trade front. Consider the fact that following the initial reciprocal tariff news in early April, the S&P 500 abruptly tanked 12% in the following four sessions, one of the most ferocious setbacks in such a period on record. It didn’t stop at stocks, as the 30-year Treasury yield leapt more than 30 bps within days, the US dollar plunged more than 4%, and even oil prices were savaged with a drop of more than $10 on fears for the global economy. Yet, in the past ten days, the US Administration has essentially resurrected those same reciprocal tariffs (in some cases even higher), and also dragged Canada and Mexico into the mix this time, and how have markets reacted? Crickets.

One could make a similar comment on the relentless assault on Fed independence and the job security of Chair Powell. Earlier this year, markets were roiled by rumours that the President was considering removing Powell. If anything, this week’s barrage was even more direct, replete with a credible source claiming that a move to fire the Chair was imminent. True, there was a brief squall in stocks and Treasuries in the middle of the week. But the tempest died down as quickly as it erupted, after the President intoned that he had no intention of firing Powell… unless there was fraud. And, then, the berating continued.

If anything, the market has not only absorbed the tough trade news, and the ceaseless Fed drama, but even rallied into it. After only the slightest of stutters on some of the tariff letters, the S&P 500 rolled to a fresh record high on Thursday, buoyed by robust bank earnings and a new high for Nvidia. Treasuries ended the week almost exactly where they began, and the US dollar has managed to strengthen in the past two weeks, even breaking above its 50-day moving average for the first time since early February.

How have markets learned to stop worrying and even love the trade war? The simple answer is that the US economy is showing remarkably few ill effects from the first wave of tariffs. While the headlines were rife this week about the trade war impact on the June CPI, the stark reality is that—so far—any tariff effect is pretty thin gruel indeed. In the past five months, which captures the start of any new tariffs, core goods prices have risen at a 0.8% annual rate. Those prices fell 1% last year, but the uptick is not going to get many hearts racing. Overall core CPI is up at a moderate 2.1% a.r. over the same period, the coolest such pace in more than four years (i.e., taking us back to before the great inflation spree). Many are warning that the inflation is still coming, since firms are working down pre-tariff inventory and/or trying to hold the line in anticipation that the trade war could de-escalate. That may still prove correct, but the overwhelming sense so far is that the inflation risk from tariffs has been wildly over-stated. And that’s even with an 8% drop in the dollar since early-year highs.

It’s a similar story on the US growth front. Despite all the dire warnings about the threat to spending and jobs from the trade war, the reality has been much more benign. True, GDP took a step back on the deep hit to net exports in Q1 on tariff front-running, but Q2 growth is still tracking in the 2% zone, scarcely concerning. After a one-month dip, consumers were right back at it in June, with retail sales popping 0.6%, and the control measure also up 0.5% (and a sturdy +4.5% y/y). If you’re looking for signs of weakness in the job market, initial claims will provide no satisfaction, having dropped five consecutive weeks to just 221,000, now below their 52-week average (of 228k). Manufacturing production also picked up in the latest month, albeit the sector is not seeing any trade windfall, with output up a modest 0.8% y/y.

How have markets learned to stop worrying and even love the trade war? The simple answer is that the US economy is showing remarkably few ill effects from the first wave of tariffs.

The flip side of a resilient economy, lingering uncertainty on the inflation front, and rollicking equity markets is that prospects for Fed easing are ebbing. Outside of Pennsylvania Avenue and Governor Waller, almost no one is expecting a cut at the July 30 meeting, but September is still in play and remains our call for the next trim. Markets are still leaning that way too, but are much less certain than even a few weeks ago. Looking further out, market pricing is roughly looking at a 25 bp cut every other meeting over the next year, close to our current assumption as well. Curiously, there doesn’t seem to be any allowance for a quickening of the pace of cuts late next spring, when (almost assuredly) a new Fed Chair will be in place. We will take the under on that call.

There is some serious symmetry for the Bank of Canada this month, as their rate decision lands on the same day as the FOMC (July 30), and Canada’s June CPI was, unusually, released at the same time as the US data. Inflation was similarly close to expectations, if not even a touch below, but not low enough to prompt the Bank to cut. Most measures of core CPI rose 0.3% m/m in s.a. terms, keeping the yearly trend stuck around 3%. So, like the Fed, there is little chance of a rate cut this month, although the heavier economic hit from the trade war means the odds are not zero. We believe that the trade chill on investment and home buying will dampen overall growth for some time yet, eventually undercutting core inflation and paving the way for additional cuts. We now look for trims in September, December and next March. If some kind of trade framework can be arranged this summer with the US, providing a morsel of clarity, we would pull one of those cuts.

Housing was back in the spotlight in Canada this week, but not always for the right reason. The latest existing home sales data revealed a modest uptick in activity for June, but with the balance still slightly favouring buyers (for a change) and prices receding further. Meantime, new condo sales continue to plumb depths not seen since the dark days of the early 1990s, suggesting that construction in that sector is facing a stall. Yet, new housing starts remained very strong above 280,000 units last month—a pace that has rarely been topped. Rental apartments have stepped into the void, keeping activity abuzz.

Even so, there was an item late this week suggesting that Ottawa was considering supporting the market, or at least wasn’t ruling out some demand side help. All we will say is… don’t go there. First, we’re never big fans of the government getting in the way of the market, absent extreme distortions. Second, overall housing affordability, while improving measurably over the past 18 months, has still got some way to go before reaching more normal levels. Getting there may require some combination of lower rates, firmer incomes (which takes time), and, yes, somewhat lower prices (at least in some markets). And, unfortunately, with the BoC on hold and Canadian bond yields backing up this week to their highest level in a year, we are going to need to lean less on rate relief and more on the latter two factors to improve affordability. But the market should be allowed to find equilibrium on its own.

Policy Contributing Writer Douglas Porter is Chief Economist for BMO.