How Canada Can Meet the China Challenge in Critical Minerals

The authors participating in the Asia Pacific Foundation of Canada panel on Canada’s Strategic Positioning in the Critical Minerals Era, September 4, 2025.

Pascale Massot and Vina Nadjibulla

September 16, 2025

Canada’s critical minerals strategy needs to move past broad ambition to systematic, prioritized, and partnership-focused action.

We need an approach that right-sizes the China challenge, adjusts to the evolving environment south of the border, embeds within a national industrial strategy, and updates our 2022 critical minerals strategy with targeted tools and deeper partnerships across the Indo-Pacific, Europe, North America, and beyond.

Critical minerals sit at the intersection of our energy transition, industrial strategy, and national security—all now shaped by the shifting dynamics of the U.S.–China relationship. Canada’s situation is unique in the world—a major resource exporter and G7 country, our economy profoundly integrated with that of the United States. We are also operating in a new environment, one that de-emphasizes globalization and economic efficiency in favour of national economic autonomy and security.

For Canada to matter, our strategy has to move with the times.

We are facing levels of economic weaponization of natural resources—the use of economic tools to achieve strategic objectives—unseen perhaps since the 1970s oil crisis. China’s new export licensing regime, unveiled on April 4th and targeting key rare-earth elements and their associated magnets, ushered in a new era of explicit leverage in critical minerals supply chains. The manufacture of permanent magnets (found in electric vehicles, aircraft, wind turbines but also computers and other electronics) is the most important use of REEs, accounting for 44% of total demand in 2022, with both demand and supply expected to grow in coming years.

Chinese approvals for magnet exports have trickled out, but the regime remains in place, and exports are tight for rare-earth elements themselves—almost none going to the United States. China’s move was both unsurprising and remarkable: we had seen the tightening of licensing or standards with little notice before, yet this time around, the breadth of impact brought large manufacturing plants to a halt at the heart of the American car industry and reverberated far beyond the United States, rattling manufacturers around the world.

The message is unmistakable: critical minerals and their associated technological ecosystems have been securitized at the highest levels in both the U.S. and China.

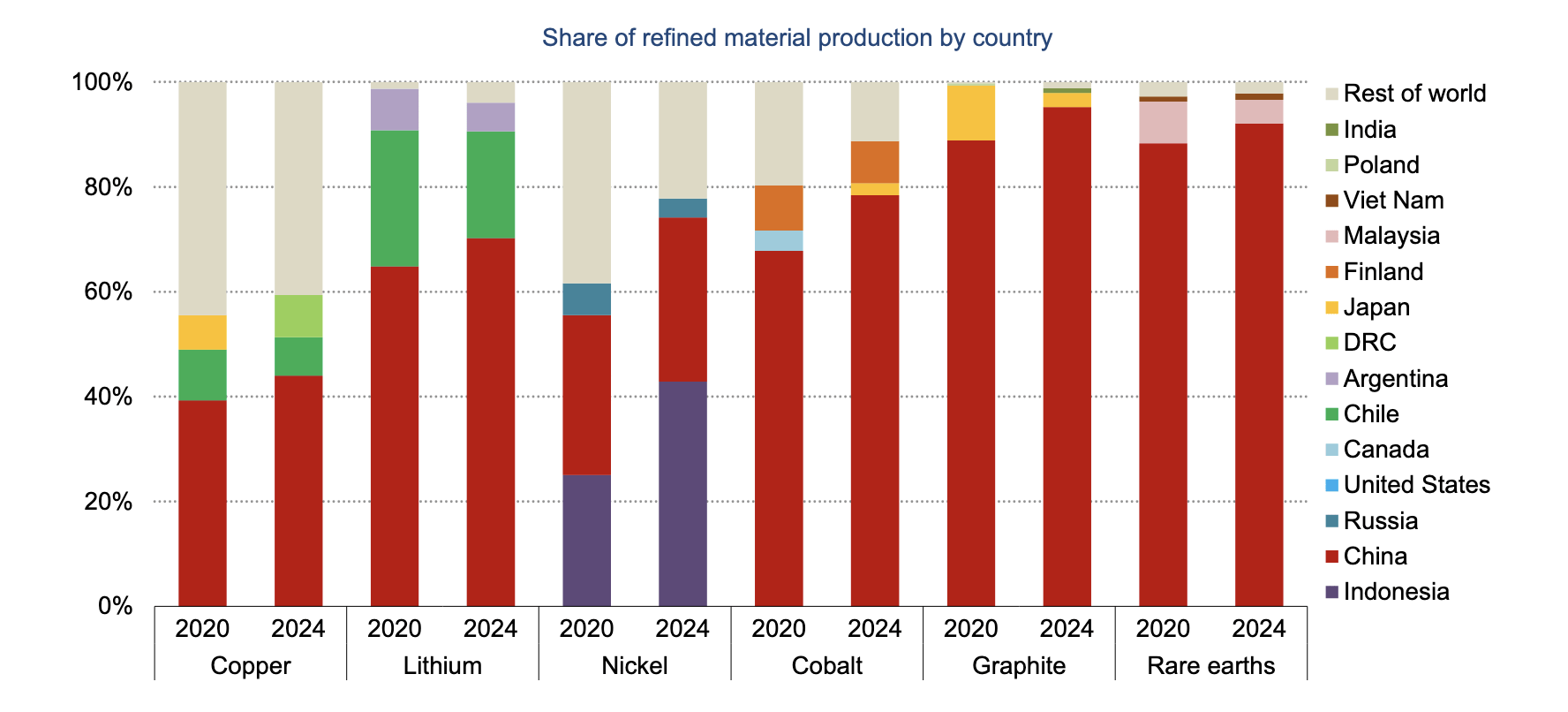

Right-sizing the China challenge means seeing both dominance and vulnerability. China has accumulated much strength in the midstream: refining and processing. It controls an average share of 70% of refining of 19 out of the 20 most important critical minerals tracked by the IEA, with rates above 90% for graphite, and rare earths. Even more striking, between 2020 and 2024, China added almost all of the growth in global refining output: cobalt (97%), rare earths (96%), graphite (98%) and even copper (83%).

But China also has exposures. It imports more than half of its needs for 19 out of 42 nonfuel minerals, including copper, cobalt and lithium, and, at the other end of the value chain, it relies on exports of manufactured goods in a world that is increasingly awake to the disruptions these can bring to domestic markets. That’s not a reason for complacency; it’s an occasion for strategy. If we pick lanes and invest in partnerships that rebalance exposure rather than try to eliminate it, competing becomes more feasible.

Partner countries are responding with instruments that go beyond sector-specific subsidies. The U.S. Department of Defence has deployed direct equity stakes and price floors (e.g. MP Materials). Australia has launched a A$ 1.2 billion mineral reserve and stockpile initiative, and its dedicated financing facility has scaled projects that otherwise would have stalled. Japan’s long-practiced approach of equity investment against long-term offtake agreements continues to secure supply, including through investments such as that in the French rare earths company CAREMAG.

The lesson for Canada is clear: others are moving fast by implementing policy steps targeting both supply and demand. Canada’s 2022 Critical Minerals Strategy set an important vision, but smaller subsidies sprinkled across a vast array of sectors—or large, one-off individual firm support—won’t get us there.

IEA Global Critical Minerals Outlook 2025

Critical minerals can only be a Canadian advantage if we: are realistic about what is feasible; specify resilience objectives; integrate this agenda within our national industrial policy; focus on creating the conditions that shape and direct economic activity rather than “picking winners”; prioritize the areas where Canada is well-positioned to make a difference; build tools through iterative dialogue with industry and other stakeholders; and work with partners whose scale and speed match the moment.

First, choices have to be made. We should stop pretending we can vertically onshore everything and instead focus on what unlocks value within global value chains. Canada is a competitive upstream producer of certain minerals, and we can credibly target parts of the midstream where clean power, our advanced manufacturing, research and services ecosystems, and ESG standards give us an edge—including by investing in process innovation, recycling, and niche advanced materials. The presence of advanced manufacturing and innovation ecosystems in Canada should be capitalized on, including with regards to the permanent magnets value chain.

Second, we should double down on standards, traceability, and pricing solutions. The G7’s emerging work on critical minerals standards is a platform Canada should lead—especially if those standards reward the real costs and benefits of clean power, labour, Indigenous partnerships and environmental stewardship. We need to provide an environment that focuses on the energy transition, recognizing that defence end-uses alone are insufficient.

Third, we need a capital stack that bites: pair supply-side policies with price-stabilization tools, mobilize our development finance institutions (DFIs) to co-anchor projects with partners’ DFIs, and think collectively about creating demand certainty where its absence is an impediment to investment.

Fourth, think ecosystems, not just sectors. To be more than the sum of its parts, a long-term vision has to incorporate what we have learned around the world about economic stewardship, including from the East Asian experience. Isolated interventions are insufficient. Systemic programs are needed that target coordination and information failures and seek to serve the public good by rewarding innovation and job creation within integrated economic ecosystems.

If this sounds like industrial strategy, that’s because it is. We cannot fully leverage this moment without integrating economic-resilience objectives within Canada’s broader industrial strategy, green shift and 4th industrial revolution ambitions—and a good-jobs/prosperity agenda for the 2020s and 2030s.

The current government is signaling that it understands the moment. The Major Projects announcement by Prime Minister Carney on September 11 targets a confluence of national interest objectives and includes projects in nuclear, minerals, electrification, transport and energy infrastructure.

To make this happen we have to look at where the growth actually is. Europe matters, but the centre of gravity is in the Indo-Pacific. The G7’s critical minerals work—importantly joined by Australia, India, and the Republic of Korea—was a good start. Now, we need to operationalize it.

With Japan and Korea, we can look at project-by-project coalitions: co-financing, offtakes, standards, connecting magnet and battery value chains. Our existing MOUs are useful only if they convert into deals with timelines and shared risk. With Australia, we should coordinate our policy tools to avoid a subsidy race that simply moves projects around the map. With India, we can move selectively but purposefully, given New Delhi’s own diversification challenges. We should not ignore Taiwan’s advanced manufacturing ecosystem, where targeted partnerships can produce resilience benefits.

Finally, China will remain an important part of global supply and value chains going forward. Like it or not, we share the common goal of each achieving resilient global supply chains. To this end, both China and the West need to build guardrails. Keeping channels of communication open is important to limit the escalatory weaponization of resources—a process that only undermines security for everyone.

All of this requires political ambition, competence and clarity.

If we move beyond generalities, and start using the right tools with the right partners, Canada can be a modern builder of economic resilience, while creating good jobs at home in a world where minerals are increasingly a lever of power.

Pascale Massot is Associate Professor in the School of Political Studies, University of Ottawa, Honorary Fellow at the Asia Society Policy Institute’s Center for China Analysis in New York and Senior Fellow at the Asia Pacific Foundation of Canada. She is also the author of China’s Vulnerability Paradox: How the World’s Largest Consumer Transformed Global Commodity Markets.

Vina Nadjibulla is the Vice-President of Research and Strategy at the Asia Pacific Foundation of Canada and an Adjunct Professor at the School of Public Policy and Global Affairs, at the University of British Columbia.