One Big, Belated Budget

Prime Minister Mark Carney and Finance Minister François-Philippe Champagne on Budget day, November 4, 2025/X

Prime Minister Mark Carney and Finance Minister François-Philippe Champagne on Budget day, November 4, 2025/X

By Robert Kavcic and Shelly Kaushik

November 4, 2025

Highlights:

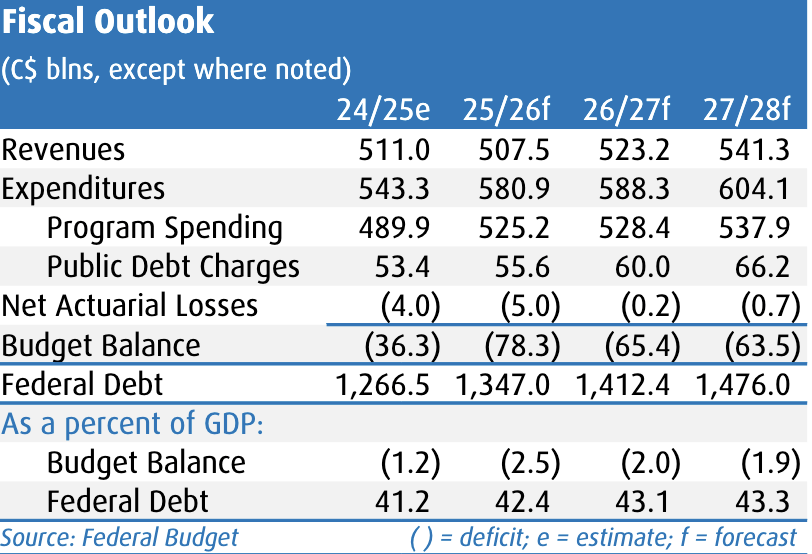

- Budget deficit of $78.3 billion in FY25/26, $65.4 billion in FY26/27.

- Debt/GDP rises to 42.4%; medium-term holds above 43%.

- Net new stimulus of $20 billion this fiscal year, mostly already announced.

- Pro-growth policy tilt with tax relief, infrastructure spending and gov’t efficiency.

- Economic assumptions subdued for 2025 and 2026 given trade uncertainty.

Overview: Short of Transformational

The highly anticipated 2025 budget lands in the middle of a trade dispute, and at a time when the Canadian economy is struggling to grow. Against that backdrop, the newly elected federal government has tabled a budget full of spending, tax relief, a push for private-sector investment, more efficient government operations, and significantly deeper deficits. Broadly, this is an economically favourable pivot from the deficit budgets run by the prior government, but also comes with what looks like a substantial structural deficit down the road. We’ll stop short of calling it transformational; and we’ll also stop short of pulling the fiscal alarm.

The FY25/26 budget deficit is estimated at $78.3 billion (2.5% of GDP), about in-line with what was expected, before narrowing somewhat to $65.4 billion (2.0% of GDP) for FY26/27. There is no path back to balance in the forecast from these levels, and deficits persist above $50 billion by FY29/30, or around 1.5% of GDP, even when the economy returns to sturdy potential growth.

Net new stimulus runs at roughly $20 billion (or about 0.6% of GDP) for FY25/26 and $22 billion for FY26/27, including the many policy measures already announced in recent months (e.g., personal income tax reduction and increased defence spending). Relative to what was already announced ahead of Budget Day, we judge that there’s roughly $4 billion (0.1% of GDP) in incremental new announcements for FY25/26 and somewhat more for FY26/27. The important takeaway here is that there is indeed a large wave of stimulus hitting the economy, but we already knew about the vast majority of it and therefore won’t be scrambling to sharply revise up our growth forecast in the wake of this budget.

Looking out over the five-year projection horizon, there is almost $90 billion of net new stimulus including recently made announcements. Of that total, roughly $36 billion is in the form of tax relief; $63 billion is in defence; $13 billion is in direct infrastructure; $28 billion is in other government spending; all of which is offset by $51 billion in government efficiency savings. Additionally, Ottawa is banking on an acceleration in private-sector investment with the aid of fast-tracked approvals across a range of projects/industries—that’s certainly encouraging, but success there will depend highly on execution.

Steep Fiscal Toll

The budget deficit is estimated at $78 billion in FY25/26 (2.5% of GDP), a sharp increase from $36 billion now expected for FY24/25 (public accounts still pending). That’s also a sharp deterioration from the $42 billion expected in the 2024 Fall Economic Statement, which was the last official projection from Ottawa. The economy has performed relatively well since that point, leaving most of the shift on the back of some tax relief and much larger spending.

For FY26/27, the budget deficit is estimated at $65 billion (2.0% of GDP). Revenues are projected to rise a solid 3.2% to $523 billion in FY26/27, led by broad gains in tax receipts, following a dip in the current fiscal year. Meantime, program spending is projected to rise a tame 0.6% after surging 7.2% in FY25/26, reflecting the many government priorities. That said, a detailed department-level efficiency effort is commendable after years of outsized growth in government operations and, if hit, the savings will be enough to offset much of the increase in defence spending. The debt-to-GDP ratio will rise to 43.1% in the coming fiscal year, from 42.4% in FY25/26, before holding above 43% through FY28/29.

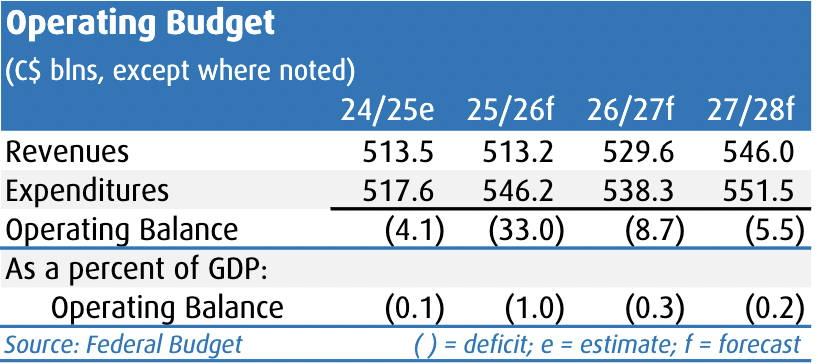

A new wrinkle is Ottawa’s presentation of separate operating and capital budgets. Note that the long-standing accounting remains in place and will be the focus for markets, so this is largely a cosmetic exercise. The operating deficit is pegged at $33 billion in FY25/26, $9 billion in FY26/27, and will be balanced by FY28/29. Two quick notes on this aspect of the budget: First, this appears to be the basis for fiscal targets, along with a declining deficit-to-GDP ratio. Also, it’s unclear how wide the net of ‘investment’ has been cast, but the sense is that several expenditures have been labelled as such to get pushed into the capital spending category, allowing operating targets to be achieved. The PBO has also noted as such, and it reinforces that this is mostly cosmetics.

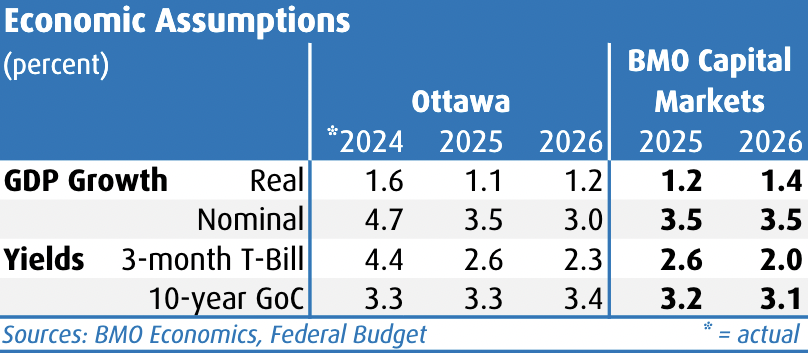

Reasonable Economic Assumptions

The budget projections are based on the private-sector consensus, but it’s a somewhat precarious one given the current unsettled state of tariffs and trade negotiations. Suffice it to say there is risk to this outlook, in both directions. The budget is based on real GDP growth of 1.1% this year (BMO Economics is at 1.2%), and 1.2% next year (1.4%). This marks a below-potential run rate into 2026 before past rate cuts and (presumably) some certainty on the trade front lend a hand. Ottawa expects nominal growth at 3.5% this year and 3.0% 2026 (we’re at 3.5% for both years). Medium term real GDP growth runs around the 2.0% mark, although potential growth could be challenged by slower population growth and ongoing productivity challenges—we’ll see if the latter can pick up the slack.

Meantime, interest rates now sit very close to what we would deem neutral, and the assumptions underlying this budget don’t diverge much from our current outlook. The 10-year yield is pegged at 3.3% this year, while the Bank of Canada is presumed to be on hold at current levels for the foreseeable future, with 3-month yields averaging around 2.5% going forward.

Summary and Market Impact

This is a big budget that opens up very large federal deficits for Canada and leaves a meaningful structural deficit down the road. However, market expectations have already anticipated these shortfalls, and it could have been worse. Talk on the Street had been as high as into the $90 billion-to-$100 billion range for the budget deficit (although we had estimated $75 billion). At the same time, the policy underlying these deficits is more palatable than those of the past decade. That is, they are built less on social spending and bigger government, and more on pro-growth measures while squeezing out some government efficiency. For a country starving for productivity growth, tax relief and a major infrastructure push are hard to dislike, although execution on the latter will matter a lot.

The bond market impact should be muted given pre-budget expectations, with perhaps some relief that the numbers weren’t worse. Bond issuance will be slightly lower in FY26/27, and not out of line with expectations. Most immediately, the stimulus announced in this budget will now get incorporated into the Bank of Canada’s near-term outlook in the January MPR. However, that’s probably already reflected in market pricing, and most of the dollars in this budget have already been known.

As such, the Canadian dollar likely doesn’t move a lot on this. Canada’s relative fiscal advantage has shrunk somewhat but remains in place. And strong execution on the investment side could actually help longer-term productivity growth. For the time being, near-term inflation trends and the evolution of the trade dispute will matter more for both yields and the loonie.

The equity market will zero in on the push to drive private-sector investment. Many industries will benefit from accelerated CCA rates, and we’ll see government push in areas like critical minerals and nuclear. The climate plan also opens the door to eliminating the oil & gas emissions cap alongside development of carbon capture.

Robert Kavcic and Shelly Kaushik are senior economists with BMO Capital Markets.